You might also like

- Dewa Bill AprilDocument1 pageDewa Bill AprilSandiego Alexander67% (3)

- FLSA Audit ProgramDocument4 pagesFLSA Audit ProgramDascalu OvidiuNo ratings yet

- Accounts Dept Audit ChecklistDocument3 pagesAccounts Dept Audit Checklistandruta1978100% (4)

- Revenue Cycle Audit Program Final 140810Document11 pagesRevenue Cycle Audit Program Final 140810Pushkar Deodhar100% (1)

- Bank Audit ProgramDocument6 pagesBank Audit Programramu9999100% (1)

- Internal Financial Control IFC Self Assessment ChecklistDocument5 pagesInternal Financial Control IFC Self Assessment ChecklistJasmine Iris Bautista100% (1)

- Bhushan Power and Steel Limited: Draft Internal Audit Report - Production and Maintenance ReviewDocument26 pagesBhushan Power and Steel Limited: Draft Internal Audit Report - Production and Maintenance ReviewJagdish MishraNo ratings yet

- Accruals Audit ProgramDocument4 pagesAccruals Audit Programvivek1119No ratings yet

- 10chap Audit Working PapersDocument10 pages10chap Audit Working PapersZahar Zahur Kaur Bhullar100% (1)

- Sarbanes Oxley Internal Controls A Complete Guide - 2021 EditionFrom EverandSarbanes Oxley Internal Controls A Complete Guide - 2021 EditionNo ratings yet

- Incoterms 2010 GuideDocument33 pagesIncoterms 2010 Guideladrillero2No ratings yet

- RCM Strategic PlanDocument20 pagesRCM Strategic PlanTubagus Donny SyafardanNo ratings yet

- Audit WorksheetDocument7 pagesAudit WorksheetEricXiaojinWangNo ratings yet

- Auditing Income Statement and Balance Sheet ItemsDocument27 pagesAuditing Income Statement and Balance Sheet ItemsNantha KumaranNo ratings yet

- Audit Programme 1Document20 pagesAudit Programme 1Neelam Goel0% (1)

- Audit ProceduresDocument5 pagesAudit ProceduresAna RetNo ratings yet

- Substantive Audit Program ARDocument3 pagesSubstantive Audit Program ARderfred00No ratings yet

- Audit ChecklistDocument44 pagesAudit Checklistwaittilldawn100% (2)

- Audit ChecklistDocument46 pagesAudit ChecklistCA Gourav Jashnani67% (3)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- K AP 3 Capital Work in ProgressDocument5 pagesK AP 3 Capital Work in Progresssibuna151No ratings yet

- Risk Based Internal Auditing in Taiwanese Banking Industry Yung MingDocument40 pagesRisk Based Internal Auditing in Taiwanese Banking Industry Yung MingGaguk M. GupronNo ratings yet

- Checklist For Statutory AuditDocument6 pagesChecklist For Statutory Auditnirav_poptani0% (1)

- Accounts Receivable, Credit and Collections Audit Report - Sample 2Document29 pagesAccounts Receivable, Credit and Collections Audit Report - Sample 2Audit Department100% (2)

- Audit Manual For CMA FirmsDocument123 pagesAudit Manual For CMA FirmsSajid Ali100% (1)

- Vendor Due Diligence Audit ProgramDocument4 pagesVendor Due Diligence Audit ProgramElla FlavierNo ratings yet

- Audit Accounts PayableDocument7 pagesAudit Accounts PayableMacmilan Trevor Jamu0% (1)

- Statutory Audit ChecklistDocument6 pagesStatutory Audit ChecklistCA SwaroopNo ratings yet

- Internal Control Manual 2016Document14 pagesInternal Control Manual 2016Marina OleynichenkoNo ratings yet

- 13 Audit Procedure For Manufacturing CompaniesDocument3 pages13 Audit Procedure For Manufacturing CompaniesManish Kumar Sukhija67% (3)

- Accured Liability Audit Work ProgramDocument2 pagesAccured Liability Audit Work ProgrammohamedciaNo ratings yet

- Fixed Asset VeificationDocument12 pagesFixed Asset Veificationnarasi64No ratings yet

- Audit Procedure of BankDocument65 pagesAudit Procedure of BankSachin Pacharne0% (1)

- Audit Program-Accrued ExpensesDocument10 pagesAudit Program-Accrued ExpensesPutu Adi NugrahaNo ratings yet

- A Report On Audit Planning of ACI LIMITEDDocument33 pagesA Report On Audit Planning of ACI LIMITEDAtiaTahiraNo ratings yet

- Audit Manual PDFDocument33 pagesAudit Manual PDFSaiful AnwarNo ratings yet

- Internal ControlDocument36 pagesInternal ControlGotta Patti HouseNo ratings yet

- Internal Audit ManualDocument7 pagesInternal Audit ManualAdolph Christian GonzalesNo ratings yet

- Internal Audit Charter and Operating StandardsDocument7 pagesInternal Audit Charter and Operating Standardssinra07No ratings yet

- Audit of Sales and ReceivablesDocument5 pagesAudit of Sales and ReceivablesTilahun S. Kura100% (1)

- Chapter 5Document22 pagesChapter 5Jenny Lelis100% (1)

- KPMG Audit OverviewDocument2 pagesKPMG Audit OverviewmynameiszooNo ratings yet

- Working Papers - Top Tips PDFDocument3 pagesWorking Papers - Top Tips PDFYus Ceballos100% (1)

- 02 Revenue Receipts Cycle Controls and Tests of ControlsDocument31 pages02 Revenue Receipts Cycle Controls and Tests of ControlsRonnelson PascualNo ratings yet

- Financial Accounting - Ch06 - Finalisation EntriesDocument13 pagesFinancial Accounting - Ch06 - Finalisation EntriesRameshKumarMuraliNo ratings yet

- Internal Control Questionnaire For SalesDocument1 pageInternal Control Questionnaire For SalesJustine Ann VillegasNo ratings yet

- Statutory Audit ModuleDocument75 pagesStatutory Audit ModulecaanusinghNo ratings yet

- Audit Program Bank and CashDocument4 pagesAudit Program Bank and CashFakhruddin Young Executives0% (1)

- Handbook On Internal AuditingDocument1 pageHandbook On Internal AuditingAshutosh100% (1)

- Topic 11 Audit of Payroll & Personnel CycleDocument14 pagesTopic 11 Audit of Payroll & Personnel Cyclebutirkuaci100% (1)

- Internal Audit ChecklistDocument44 pagesInternal Audit ChecklistGlenn Padilla100% (3)

- Project On Audit Plan and Programme & Special AuditDocument11 pagesProject On Audit Plan and Programme & Special AuditPriyank SolankiNo ratings yet

- Implementation Guide On ICFR PDFDocument67 pagesImplementation Guide On ICFR PDFVimal KumarNo ratings yet

- Cost Audit PDFDocument37 pagesCost Audit PDFAl Amin Sarkar0% (1)

- Audit Risk and Internal ControlDocument17 pagesAudit Risk and Internal ControlAlexandru VasileNo ratings yet

- Chapter 19 - Test of ControlDocument22 pagesChapter 19 - Test of ControlJhenna ValdecanasNo ratings yet

- Procurement IcqDocument8 pagesProcurement IcqzuldvsbNo ratings yet

- Audit of Fixed Assets 1Document3 pagesAudit of Fixed Assets 1Leon MushiNo ratings yet

- Internal Audit ChecklistDocument80 pagesInternal Audit ChecklistdinuindiaNo ratings yet

- Bai Type Code GuideDocument31 pagesBai Type Code Guideswathipotla100% (1)

- Warehousing Logistics Storage Services Lucknow by WEDocument3 pagesWarehousing Logistics Storage Services Lucknow by WEGurjeet SinghNo ratings yet

- Incoterms 2010Document2 pagesIncoterms 2010AMBYNo ratings yet

- Renewal Notice: Policy No.P/141126/01/2019/003974Document1 pageRenewal Notice: Policy No.P/141126/01/2019/003974manoharNo ratings yet

- Transport ModeDocument5 pagesTransport ModeDrinkwell AccountsNo ratings yet

- 7 PsDocument7 pages7 PsChristine LlorenNo ratings yet

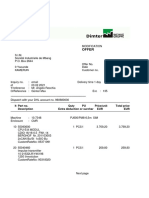

- Offer: It Part No. Quty PU Price/unit Total Price Description Extra Deduction or Surchar EUR EURDocument3 pagesOffer: It Part No. Quty PU Price/unit Total Price Description Extra Deduction or Surchar EUR EURMichelNo ratings yet

- Bank StatementsDocument14 pagesBank StatementsDanielle Ann OreaNo ratings yet

- Account Statement 190523 020623Document11 pagesAccount Statement 190523 020623aditya MauryaNo ratings yet

- Supply Chain Management-Historical PerspectiveDocument7 pagesSupply Chain Management-Historical PerspectiveTalha SaeedNo ratings yet

- University of Nueva Caceres College of Business and Accountancy J. Hernandez Avenue, Naga City Prelim Exam Intermediate Accounting One JdmanaogDocument10 pagesUniversity of Nueva Caceres College of Business and Accountancy J. Hernandez Avenue, Naga City Prelim Exam Intermediate Accounting One JdmanaogJustin ManaogNo ratings yet

- Statement of Account: Credit Limit Rs Available Credit Limit RsDocument2 pagesStatement of Account: Credit Limit Rs Available Credit Limit RsIqbal MohammadNo ratings yet

- Rebate: Due DateDocument2 pagesRebate: Due DateRakesh Dey sarkarNo ratings yet

- NOTEDocument9 pagesNOTEkatieNo ratings yet

- Modern Road Makers Private Limited: Po No: PO DateDocument2 pagesModern Road Makers Private Limited: Po No: PO DateSuryasai RednamNo ratings yet

- E-Service Complaint FormDocument1 pageE-Service Complaint FormGbadeyanka O WuraolaNo ratings yet

- Transaction Date Value Date Cheque Number/ Transaction Number Description Debit Credit Running BalanceDocument3 pagesTransaction Date Value Date Cheque Number/ Transaction Number Description Debit Credit Running BalancejyothiNo ratings yet

- Q-Arsi-0319-0868 EmailDocument4 pagesQ-Arsi-0319-0868 EmailDimasBagusRukhmantiarnoNo ratings yet

- XXXXXXX 1029Document18 pagesXXXXXXX 1029Jamaluddin GauriNo ratings yet

- XboxDocument6 pagesXboxvenipaz63No ratings yet

- Non-Individual Taxation: 1. Corporations 2. Co-Ownership 3. Estates and Trusts 4. PartnershipsDocument58 pagesNon-Individual Taxation: 1. Corporations 2. Co-Ownership 3. Estates and Trusts 4. PartnershipsShiela Marie Vics60% (5)

- Tally AssignmentDocument26 pagesTally AssignmentPravah Shukla80% (65)

- Cash and Internal ControlDocument47 pagesCash and Internal ControlHEM CHEA100% (2)

- Haroon Sharif S/O M. Sharif Bhatti 152-Pak Block A I Town: Web Generated BillDocument1 pageHaroon Sharif S/O M. Sharif Bhatti 152-Pak Block A I Town: Web Generated BillHamza KhanNo ratings yet

- Monzo Bank Statement 2020 12 01-2020 12 31 8417Document27 pagesMonzo Bank Statement 2020 12 01-2020 12 31 8417Vitor BinghamNo ratings yet

- VAT ReviewDocument8 pagesVAT ReviewabbyNo ratings yet

- Proforma of Reimbursement of Tution FeesDocument1 pageProforma of Reimbursement of Tution FeesswethaNo ratings yet