You might also like

- HDFC Bank CAMELS Analysis and DuPont ModelDocument31 pagesHDFC Bank CAMELS Analysis and DuPont Modelasifbhaiyat33% (3)

- A Case Study of Profitability Analysis of Standard Chartered Bank Nepal LTDDocument16 pagesA Case Study of Profitability Analysis of Standard Chartered Bank Nepal LTDDiwesh Tamrakar100% (1)

- A Case Study of Profitability Analysis of Standard Chartered Bank Nepal LTDDocument16 pagesA Case Study of Profitability Analysis of Standard Chartered Bank Nepal LTDram binod yadavNo ratings yet

- Camels Model AnalysisDocument11 pagesCamels Model AnalysisAlbert SmithNo ratings yet

- Performance Evaluation of Banks Through CAMELS FRAMEWORKDocument54 pagesPerformance Evaluation of Banks Through CAMELS FRAMEWORKAnshuman Singh79% (24)

- Camel Rating (Framework) of Four BanksDocument94 pagesCamel Rating (Framework) of Four Bankslovels_agrawal631387% (23)

- LIQUIDITY RISK AND LIQUIDITY MANAGEMENT IN ISLAMIC BANKS (DR Salman)Document29 pagesLIQUIDITY RISK AND LIQUIDITY MANAGEMENT IN ISLAMIC BANKS (DR Salman)lahem88100% (4)

- A CAMEL MODEL ANALYSIS OF PUBLIC & PRIVATE SECTOR BANKS IN INDIACamels Rating PDFDocument23 pagesA CAMEL MODEL ANALYSIS OF PUBLIC & PRIVATE SECTOR BANKS IN INDIACamels Rating PDFsambhu_n100% (1)

- Financial Statement Analysis of ICICI Bank and A Comparative Study With Axis BankDocument7 pagesFinancial Statement Analysis of ICICI Bank and A Comparative Study With Axis Banksridharkar06100% (1)

- HDFC Bank StrategyDocument214 pagesHDFC Bank StrategyMukul Yadav0% (1)

- CAMEL Analysis For Indian BanksDocument10 pagesCAMEL Analysis For Indian BanksAbhishek Anand75% (4)

- Camel ThesisDocument97 pagesCamel ThesisSadhana Joshi63% (8)

- Analysis of The Investment Modes of First Security Islamic Bank LTDDocument80 pagesAnalysis of The Investment Modes of First Security Islamic Bank LTDAbid H Rahat50% (10)

- Camel ModelDocument10 pagesCamel ModelHarsha ChowdharyNo ratings yet

- Indian Financial System-Kalyani DuttaDocument63 pagesIndian Financial System-Kalyani Duttakalyanidutta0% (1)

- Maximum Permissible Bank Finance PDFDocument7 pagesMaximum Permissible Bank Finance PDFitrrustNo ratings yet

- Pricing of Financial Products and Services Offered by BankDocument42 pagesPricing of Financial Products and Services Offered by BankSmitaNo ratings yet

- Technology Enabled Transformation in Banking 2011Document28 pagesTechnology Enabled Transformation in Banking 2011Gunay88No ratings yet

- Capital Market in IndiaDocument60 pagesCapital Market in IndiaR Rabi ReddyNo ratings yet

- HDFC Bank CAMELS AnalysisDocument15 pagesHDFC Bank CAMELS Analysisprasanthgeni22No ratings yet

- Final Camels FrameworkDocument75 pagesFinal Camels FrameworkParth ShahNo ratings yet

- Capital Adequacy Analysis of Top Bangladeshi BanksDocument10 pagesCapital Adequacy Analysis of Top Bangladeshi BanksFaysal KhanNo ratings yet

- Branchless Banking Project ReportDocument70 pagesBranchless Banking Project ReportAnsarAnsariNo ratings yet

- Impact of Liquidity on Bank ProfitsDocument12 pagesImpact of Liquidity on Bank ProfitsRajesh ShresthaNo ratings yet

- Banking Sector ReformsDocument27 pagesBanking Sector ReformsArghadeep ChandaNo ratings yet

- The Effects of Deposits Mobilization On Financial Performance in Commercial Banks in Rwanda. A Case of Equity Bank Rwanda Limited PDFDocument28 pagesThe Effects of Deposits Mobilization On Financial Performance in Commercial Banks in Rwanda. A Case of Equity Bank Rwanda Limited PDFJohn FrancisNo ratings yet

- Consortium BankingDocument4 pagesConsortium BankingSnigdha DasNo ratings yet

- A Study On Credit Appraisal System On SME of Union Bank of IndiaDocument56 pagesA Study On Credit Appraisal System On SME of Union Bank of IndiaSarva ShivaNo ratings yet

- Causes of NPADocument7 pagesCauses of NPAsggovardhan0% (1)

- Corporate Dividend Policy A Study Commercial Banks of Nepal PDFDocument21 pagesCorporate Dividend Policy A Study Commercial Banks of Nepal PDFYog Raj RijalNo ratings yet

- ALM in BanksDocument65 pagesALM in BanksrockpdNo ratings yet

- Creative Analysis of Financial ReportDocument31 pagesCreative Analysis of Financial ReportHitesh PatelNo ratings yet

- Literature Review For Profitability Analysis of Public Sector BanksDocument2 pagesLiterature Review For Profitability Analysis of Public Sector Bankskarthut100% (4)

- Quality reports and business consultancy solutions for boosting organizational performanceDocument54 pagesQuality reports and business consultancy solutions for boosting organizational performanceshoaib.xctvz2122No ratings yet

- The Financial Analysis of Himalyan Bank ComDocument28 pagesThe Financial Analysis of Himalyan Bank ComSushil Paudel100% (1)

- Axis Bank: A Study on Operations and FinacleDocument50 pagesAxis Bank: A Study on Operations and FinacleHarnaman SinghNo ratings yet

- OB Union BankDocument6 pagesOB Union BankArka Goswami100% (1)

- Introduction of Banking SectorDocument6 pagesIntroduction of Banking SectorPatel Binny50% (2)

- Internship Report On Global Ime Bank LimDocument32 pagesInternship Report On Global Ime Bank LimManju MaharaNo ratings yet

- Chapter - 01 Introduction of BankDocument37 pagesChapter - 01 Introduction of BankJeeva JeevaNo ratings yet

- Ratio Analysis ProjectDocument40 pagesRatio Analysis ProjectAnonymous g7uPednINo ratings yet

- For HDFC BankDocument31 pagesFor HDFC BankShalu Sushil Bansal80% (5)

- Innovation in Banking SectorDocument4 pagesInnovation in Banking SectorHetvi RajanNo ratings yet

- Case Study NPADocument3 pagesCase Study NPAGulshan KumarNo ratings yet

- A Case Study of Financial Analysis of Nepal SDocument22 pagesA Case Study of Financial Analysis of Nepal SDiwesh Tamrakar100% (1)

- Investment BankingDocument16 pagesInvestment BankingSudarshan DhavejiNo ratings yet

- Capital Adequacy Presentation 1Document16 pagesCapital Adequacy Presentation 1Nafiz Imran DiptoNo ratings yet

- Submitted By: Project Submitted in Partial Fulfillment For The Award of Degree ofDocument9 pagesSubmitted By: Project Submitted in Partial Fulfillment For The Award of Degree ofMOHAMMED KHAYYUMNo ratings yet

- A Case Study On Credit Appraisal For Working Capital Finance To Small and Medium Enterprises in Bank of IndiaDocument34 pagesA Case Study On Credit Appraisal For Working Capital Finance To Small and Medium Enterprises in Bank of Indiaarcherselevators0% (1)

- 205 - F - Icici-A Study On Credit Appraisal System at Icici BankDocument71 pages205 - F - Icici-A Study On Credit Appraisal System at Icici BankPeacock Live Projects0% (1)

- Working Capital Management and Its Impact On Profitability Evidence From Food Complex Manufacturing Firms in Addis AbabaDocument19 pagesWorking Capital Management and Its Impact On Profitability Evidence From Food Complex Manufacturing Firms in Addis AbabaJASH MATHEWNo ratings yet

- Footwear Industry and Bay Emporium AnalysisDocument9 pagesFootwear Industry and Bay Emporium AnalysisTaisir Mahmud0% (1)

- Economics Project 2NEWDocument8 pagesEconomics Project 2NEWmukilanmukilan284No ratings yet

- Panjab National BankDocument9 pagesPanjab National BankVivid Geo BabuNo ratings yet

- Competitor BanksDocument6 pagesCompetitor BanksAshish KumarNo ratings yet

- SAMIMADocument37 pagesSAMIMASamima ShaikhNo ratings yet

- Introduction of Pnb,,,Improved FileDocument10 pagesIntroduction of Pnb,,,Improved FileJitin BhutaniNo ratings yet

- HDFC Bank-Report-Project On PerceptionDocument98 pagesHDFC Bank-Report-Project On PerceptionRajeev GuptaNo ratings yet

- Bhavesh Jhala 1 PDFDocument42 pagesBhavesh Jhala 1 PDFAniket AutkarNo ratings yet

- Meet Mate INTM ProjectDocument22 pagesMeet Mate INTM ProjectSrikanth Kumar KonduriNo ratings yet

- Panel Data Analysis: Indian Pharmacy IndustryDocument11 pagesPanel Data Analysis: Indian Pharmacy IndustrySrikanth Kumar KonduriNo ratings yet

- At&T - Equity Research ReportDocument12 pagesAt&T - Equity Research ReportSrikanth Kumar Konduri0% (1)

- Summer Project Report Srikanth 10FN-109Document36 pagesSummer Project Report Srikanth 10FN-109Srikanth Kumar KonduriNo ratings yet

- Erp V4Document37 pagesErp V4Srikanth Kumar KonduriNo ratings yet

- FSABV Final ReportDocument3 pagesFSABV Final ReportSrikanth Kumar KonduriNo ratings yet

- Durban Summit 2011 - EnVM Project Report - Sec.GDocument8 pagesDurban Summit 2011 - EnVM Project Report - Sec.GSrikanth Kumar KonduriNo ratings yet

- Final PPT of MarutiDocument21 pagesFinal PPT of MarutiSrikanth Kumar KonduriNo ratings yet

- IREF Project ReportDocument10 pagesIREF Project ReportSrikanth Kumar KonduriNo ratings yet

- FIS Empirical Project Macro Factors Vs Yield CurveDocument2 pagesFIS Empirical Project Macro Factors Vs Yield CurveSrikanth Kumar KonduriNo ratings yet

- QMM 2nd Assignment 10FN-109Document3 pagesQMM 2nd Assignment 10FN-109Srikanth Kumar KonduriNo ratings yet

- Trading StrategyDocument1 pageTrading StrategySrikanth Kumar KonduriNo ratings yet

- Wintel AnalysisDocument11 pagesWintel AnalysisSrikanth Kumar Konduri100% (2)

- MACR Igate Patni Ver4.0Document14 pagesMACR Igate Patni Ver4.0Srikanth Kumar KonduriNo ratings yet

- Bitc Mfi ProjectDocument13 pagesBitc Mfi ProjectSrikanth Kumar KonduriNo ratings yet

- Tailor-Made Portfolio Design Using Markowitz Efficient Frontier ThoeryDocument3 pagesTailor-Made Portfolio Design Using Markowitz Efficient Frontier ThoerySrikanth Kumar KonduriNo ratings yet

- IB - Doing Business in China - 2011Document27 pagesIB - Doing Business in China - 2011Srikanth Kumar KonduriNo ratings yet

- Modeling of Risk Using Monte Carlo SimulationDocument16 pagesModeling of Risk Using Monte Carlo SimulationSrikanth Kumar KonduriNo ratings yet

- TVS Motors ValuationDocument2 pagesTVS Motors ValuationSrikanth Kumar KonduriNo ratings yet

- Strategic HRM - SecGDocument20 pagesStrategic HRM - SecGSrikanth Kumar KonduriNo ratings yet

- Escorts Optimization of ProductionDocument20 pagesEscorts Optimization of ProductionSrikanth Kumar KonduriNo ratings yet

- Camel Ratio AnalysisDocument15 pagesCamel Ratio AnalysisSrikanth Kumar Konduri90% (10)

- Prevention of Oppression & Mismanagement - Group04 - Sec.G - LAB2011 - IMTGDocument29 pagesPrevention of Oppression & Mismanagement - Group04 - Sec.G - LAB2011 - IMTGSrikanth Kumar KonduriNo ratings yet

- Spyder Active Sports Case AnalysisDocument2 pagesSpyder Active Sports Case AnalysisSrikanth Kumar Konduri100% (3)

- Dividend Policy at Linear Technology - Case Analysis - G05Document2 pagesDividend Policy at Linear Technology - Case Analysis - G05Srikanth Kumar Konduri60% (5)

- LPO in IndiaDocument14 pagesLPO in IndiaSrikanth Kumar KonduriNo ratings yet

- Dell's Working Capital - Case Analysis - G05Document2 pagesDell's Working Capital - Case Analysis - G05Srikanth Kumar Konduri100% (11)

- BRM Project - Currency Derivatives Trading - Lighter VersionDocument30 pagesBRM Project - Currency Derivatives Trading - Lighter VersionSrikanth Kumar KonduriNo ratings yet

- Adarsh Cooperative Housing Society ScamDocument14 pagesAdarsh Cooperative Housing Society ScamSrikanth Kumar KonduriNo ratings yet

- BC-2 Interaction With Foreign ClientsDocument24 pagesBC-2 Interaction With Foreign ClientsSrikanth Kumar KonduriNo ratings yet

- About CimbDocument7 pagesAbout CimbShahmin HalimiNo ratings yet

- KIBOR As Of: Treasury Contact NumbersDocument1 pageKIBOR As Of: Treasury Contact NumbersMuhammad Ashraf YousufNo ratings yet

- Statement of HSBC Pulse Unionpay Dual Currency Diamond Card PulseDocument6 pagesStatement of HSBC Pulse Unionpay Dual Currency Diamond Card PulseCova ChanNo ratings yet

- HDFC Bank's Mission as a World Class Indian BankDocument24 pagesHDFC Bank's Mission as a World Class Indian BankYogi GandhiNo ratings yet

- 1627224741350Document26 pages1627224741350Vasudha VasudevNo ratings yet

- Hkex New Entrusted Loan Arrangement 信达国际Document9 pagesHkex New Entrusted Loan Arrangement 信达国际Martin JpNo ratings yet

- Banking Regulation and Structure in IndiaDocument69 pagesBanking Regulation and Structure in IndiaShaifali ChauhanNo ratings yet

- RHB BankDocument24 pagesRHB Bankirfan sururi100% (1)

- BofA Q2 2022Document37 pagesBofA Q2 2022ZerohedgeNo ratings yet

- Answer Chapter 1Document5 pagesAnswer Chapter 1Nguyễn Châu Mỹ KiềuNo ratings yet

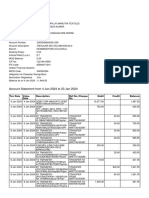

- Account Statement From 4 Jan 2024 To 23 Jan 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 4 Jan 2024 To 23 Jan 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancerangaswamy8194No ratings yet

- Pro Forma PDFDocument1 pagePro Forma PDFtvsufi.comNo ratings yet

- Main Acct Statemetn Jan To Dec 18Document8 pagesMain Acct Statemetn Jan To Dec 18Col RajNo ratings yet

- Credit Agricole - SWOTDocument1 pageCredit Agricole - SWOTMandula KumarasinghaNo ratings yet

- Nondeliverable Forward enDocument2 pagesNondeliverable Forward enPushpraj Singh BaghelNo ratings yet

- MCB Final ReportDocument17 pagesMCB Final ReportkamranNo ratings yet

- Discounted Interest and Compounding InterestDocument4 pagesDiscounted Interest and Compounding Interestmizpah mae jolitoNo ratings yet

- Account Statement: Gedung Arthaloka Jl. Jenderal Sudirman Kav 2, Jakarta 10220, IndonesiaDocument8 pagesAccount Statement: Gedung Arthaloka Jl. Jenderal Sudirman Kav 2, Jakarta 10220, IndonesiaAnonymous TgF9oINo ratings yet

- Invoice Flomih & Vio Bussines SRL: CX Ref: 18911926 Invoice No.: 151140-838 Invoice Date: 29 Nov 2019Document1 pageInvoice Flomih & Vio Bussines SRL: CX Ref: 18911926 Invoice No.: 151140-838 Invoice Date: 29 Nov 2019calinmusceleanuNo ratings yet

- Acct Statement - XX0575 - 21052022Document4 pagesAcct Statement - XX0575 - 21052022shivji007No ratings yet

- Bank of Kigali Announces Q2 2011 & 1H 2011 ResultsDocument9 pagesBank of Kigali Announces Q2 2011 & 1H 2011 ResultsBank of KigaliNo ratings yet

- N SKTQK 7 DV Ev LFSMaDocument3 pagesN SKTQK 7 DV Ev LFSMas/gfoergNo ratings yet

- Annual Report On Basic BankDocument81 pagesAnnual Report On Basic BankDipock Mondal0% (1)

- Background of The Study and Related LiteratureDocument5 pagesBackground of The Study and Related LiteratureJohn Andrae MangloNo ratings yet

- The Relationship Between Exchange Rates Swap Spreads and Mortgage SpreadsDocument27 pagesThe Relationship Between Exchange Rates Swap Spreads and Mortgage Spreadsbuckybad2No ratings yet

- Credit Card Generator & Validator - Valid Visa Numbers - CardGuruDocument10 pagesCredit Card Generator & Validator - Valid Visa Numbers - CardGuruJelo BagzNo ratings yet

- Credit Union EssayDocument2 pagesCredit Union EssayInday MiraNo ratings yet

- Eoif Working Capital FinanceDocument16 pagesEoif Working Capital Financeengr_asad364No ratings yet

- Answers To Some Important Questions Asked in The BB Viva Board in 2017Document21 pagesAnswers To Some Important Questions Asked in The BB Viva Board in 2017shopno100% (1)

- Schedule of Charges PDFDocument3 pagesSchedule of Charges PDFSrinivas MadyalaNo ratings yet