You might also like

- Berrett v. Elmo, 4th Cir. (1999)Document3 pagesBerrett v. Elmo, 4th Cir. (1999)Scribd Government Docs100% (1)

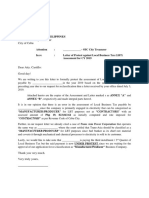

- Business Tax Protest LetterDocument2 pagesBusiness Tax Protest LetterCoco Loco73% (15)

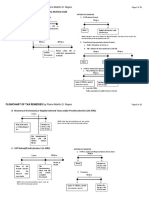

- Flowchart of Tax Remedies I. Remedies UnDocument12 pagesFlowchart of Tax Remedies I. Remedies UnKevin Ken Sison Ganchero100% (2)

- David Robinson LawsuitDocument105 pagesDavid Robinson LawsuitThe Salt Lake TribuneNo ratings yet

- 7 Sure-Ways To Cancel Bir Letters of AuthorityDocument2 pages7 Sure-Ways To Cancel Bir Letters of Authorityjuliet_emelinotmaestro90% (10)

- Tax Flowchart Remedies (Tokie)Document9 pagesTax Flowchart Remedies (Tokie)Tokie TokiNo ratings yet

- Lopez V Pan Am World AirwaysDocument3 pagesLopez V Pan Am World Airwaysmnyng100% (1)

- CTA and Taxpayers Remedies-2020Document66 pagesCTA and Taxpayers Remedies-2020Agui S. T. PadNo ratings yet

- Bir Ruling Da 081 03Document2 pagesBir Ruling Da 081 03CzarPaguio100% (1)

- Revenue Regulations No 12-99Document3 pagesRevenue Regulations No 12-99Zoe Dela CruzNo ratings yet

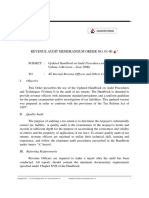

- RMO No. 7-2015 PDFDocument2 pagesRMO No. 7-2015 PDFChristopher Johnson100% (2)

- ProtestLetter TICIDocument4 pagesProtestLetter TICIdbircs100% (4)

- Rmo 20-90Document2 pagesRmo 20-90cmv mendoza100% (3)

- Ramo 1-00Document186 pagesRamo 1-00dan2aurusNo ratings yet

- RR 12-1999Document21 pagesRR 12-1999anorith8867% (6)

- Ramo 1-2000Document177 pagesRamo 1-2000Kris Calabia100% (2)

- Writ of Amparo SampleDocument9 pagesWrit of Amparo SampleCharlotte GallegoNo ratings yet

- Bir RR 12-99Document7 pagesBir RR 12-99Cha AgaderNo ratings yet

- Rmo 43-90 PDFDocument5 pagesRmo 43-90 PDFRieland Cuevas67% (3)

- Banda VS ErmitaDocument2 pagesBanda VS ErmitaCheska Christiana Villarin SaguinNo ratings yet

- Abci V Cir DigestDocument9 pagesAbci V Cir DigestSheilaNo ratings yet

- Preliminary Assessment NoticeDocument2 pagesPreliminary Assessment NoticeHanabishi RekkaNo ratings yet

- PetitionDocument6 pagesPetitionmarie kris100% (2)

- Alonzo V ConcepcionDocument3 pagesAlonzo V ConcepcioniciamadarangNo ratings yet

- Trust 1Document112 pagesTrust 1mnyngNo ratings yet

- Hon. Caesar R. Dulay Bureau of Internal Revenue: CommissionerDocument4 pagesHon. Caesar R. Dulay Bureau of Internal Revenue: CommissionerPatrice Noelle Ramirez90% (10)

- Best Evidence Obtainable in The Realm of The Phil. Tax CodeDocument4 pagesBest Evidence Obtainable in The Realm of The Phil. Tax Codehenzencamero100% (1)

- RR 2-98Document3 pagesRR 2-98mnyng100% (3)

- Midwifery LawDocument4 pagesMidwifery LawKathryn Kaye Carpio67% (3)

- Philippine Bank of Communications Vs Commissioner of Internal RevenueDocument2 pagesPhilippine Bank of Communications Vs Commissioner of Internal RevenueNFNL100% (1)

- Sample-Notice of GarnishmentDocument13 pagesSample-Notice of GarnishmentVon Greggy Moloboco IINo ratings yet

- Rmo 1-90Document14 pagesRmo 1-90cmv mendoza100% (2)

- BIR Ruling (DA - (C-066) 228-09) - Capital Infusion in The Form of APIC Not Subject To Donor's TaxDocument8 pagesBIR Ruling (DA - (C-066) 228-09) - Capital Infusion in The Form of APIC Not Subject To Donor's TaxJerwin Dave100% (1)

- RR 2-98Document85 pagesRR 2-98restless11No ratings yet

- 590657Document202 pages590657Bhaskar100% (2)

- Self Organisation.+Counter Economic StrategiesDocument168 pagesSelf Organisation.+Counter Economic StrategiesLee Jae-Won100% (1)

- Compromise of BIR Tax LiabilityDocument2 pagesCompromise of BIR Tax LiabilityIssaRoxas100% (2)

- November 20, 2017 G.R. No. 226454 DIGNA RAMOS, Petitioner People of The Philippines, Respondent Decision Perlas-Bernabe, J.Document7 pagesNovember 20, 2017 G.R. No. 226454 DIGNA RAMOS, Petitioner People of The Philippines, Respondent Decision Perlas-Bernabe, J.Frederick EboñaNo ratings yet

- Archbishop Reyes Ave, Cebu City, Cebu, 6000Document5 pagesArchbishop Reyes Ave, Cebu City, Cebu, 6000Ralf Arthur Silverio100% (1)

- RR 12-99 Full TextDocument5 pagesRR 12-99 Full TextErmawoo100% (2)

- Business Tax Protest Letter SampleDocument1 pageBusiness Tax Protest Letter SampleMaristela Regidor100% (1)

- Philpost RRDocument6 pagesPhilpost RRGene AbotNo ratings yet

- Digest of Ramsay vs. CIR, CTA Case No. 8456, September 17, 2015Document2 pagesDigest of Ramsay vs. CIR, CTA Case No. 8456, September 17, 2015Michael Joseph NogoyNo ratings yet

- RemediesDocument45 pagesRemediesCzarina100% (1)

- Bureau of Internal Revenue: Deficiency Tax AssessmentDocument9 pagesBureau of Internal Revenue: Deficiency Tax AssessmentXavier Cajimat UrbanNo ratings yet

- RMC 46-99Document7 pagesRMC 46-99mnyng100% (1)

- Affidavit of Desistance OmbudsmanDocument3 pagesAffidavit of Desistance OmbudsmanNinJj Mac100% (1)

- BIR Ruling (DA - (C-005) 023-08) (Condonation of Debt)Document5 pagesBIR Ruling (DA - (C-005) 023-08) (Condonation of Debt)Archie Guevarra100% (3)

- Dof Order No. 149-95Document1 pageDof Order No. 149-95matinikkiNo ratings yet

- Rdao 05-01Document3 pagesRdao 05-01cmv mendoza100% (1)

- Tupas v. NHADocument2 pagesTupas v. NHARaymond Roque100% (1)

- Bir Waiver of Defense of PrescriptionDocument3 pagesBir Waiver of Defense of PrescriptionCha Ancheta Cabigas0% (1)

- Bir Ruling No. 1243-18 - JvsDocument3 pagesBir Ruling No. 1243-18 - Jvsjohn allen MarillaNo ratings yet

- Tax 2 Case Digests Part 2 Transfer Taxes PDFDocument25 pagesTax 2 Case Digests Part 2 Transfer Taxes PDFNolaida AguirreNo ratings yet

- Kepco Vs CIR Case DigestDocument2 pagesKepco Vs CIR Case DigestFrancisca Paredes100% (1)

- Tax 2 Digest (0406) GR 108576 012099 Cir Vs CaDocument3 pagesTax 2 Digest (0406) GR 108576 012099 Cir Vs CaAudrey Deguzman100% (1)

- Substantial EvidenceDocument15 pagesSubstantial EvidenceArahbells100% (1)

- People Vs BalagtasDocument2 pagesPeople Vs BalagtasBilly100% (2)

- 22.d CIR vs. BPI (G.R. No. 178490 July 7, 2009) - H DigestDocument2 pages22.d CIR vs. BPI (G.R. No. 178490 July 7, 2009) - H DigestHarleneNo ratings yet

- NGCP Vs Ofelia Oliva (GR No. 213157, 2016) - Taxation Law DigestDocument1 pageNGCP Vs Ofelia Oliva (GR No. 213157, 2016) - Taxation Law DigestJCNo ratings yet

- Sample PANDocument5 pagesSample PANArmie Lyn Simeon100% (1)

- RMC 101-90Document2 pagesRMC 101-90Latasha Phillips100% (2)

- Systra Phils Inc v. CIRDocument1 pageSystra Phils Inc v. CIRBRYAN JAY NUIQUENo ratings yet

- Dof Order No 137 87 PDFDocument7 pagesDof Order No 137 87 PDFAilmore BautistaNo ratings yet

- SEC Consolidated Scale of Fines 05 Nov 2013 (26 Nov 2013)Document124 pagesSEC Consolidated Scale of Fines 05 Nov 2013 (26 Nov 2013)Katrina Ross Manzano100% (4)

- Sample Protest LetterDocument2 pagesSample Protest LetterConsciousness Vivid100% (1)

- Rmo 62-99Document6 pagesRmo 62-99Klaters BokuNo ratings yet

- Vda. de San Agustin Vs CIRDocument9 pagesVda. de San Agustin Vs CIRKevin MatibagNo ratings yet

- General Audit Procedures and Documentation-BirDocument3 pagesGeneral Audit Procedures and Documentation-BirAnalyn BanzuelaNo ratings yet

- RR 16-99Document6 pagesRR 16-99matinikkiNo ratings yet

- Assessment DueprocessDocument2 pagesAssessment DueprocessRester NonatoNo ratings yet

- Tax Law 1 DG3 NOTES Part 2Document28 pagesTax Law 1 DG3 NOTES Part 2Fayie De LunaNo ratings yet

- TopicsDocument40 pagesTopicsDa Yani ChristeeneNo ratings yet

- Dispute of Assessment - WongDocument5 pagesDispute of Assessment - WongAnne Fatima PilayreNo ratings yet

- 1Document1 page1Jj YuviencoNo ratings yet

- Report Excel FormatDocument1 pageReport Excel FormatmnyngNo ratings yet

- Sottomayer, Otherwise de Barros V. de Barros (The Queen'S Proctor Intervening)Document9 pagesSottomayer, Otherwise de Barros V. de Barros (The Queen'S Proctor Intervening)mnyngNo ratings yet

- Remedies Under The Tax Code of 1997Document7 pagesRemedies Under The Tax Code of 1997mnyngNo ratings yet

- Ibp Journal Vol.34 No.2 2009Document155 pagesIbp Journal Vol.34 No.2 2009mnyngNo ratings yet

- Some Tax CasesDocument5 pagesSome Tax CasesmnyngNo ratings yet

- RR 3-91Document3 pagesRR 3-91mnyngNo ratings yet

- Ong PoDocument1 pageOng PomnyngNo ratings yet

- Taxrev 3.7.11Document99 pagesTaxrev 3.7.11mnyngNo ratings yet

- Rallos vs. Felix Go Chan & Sons Realty Corp. 81 SCRA 251 - G.R. No. L-24332 - January 31, 1978Document9 pagesRallos vs. Felix Go Chan & Sons Realty Corp. 81 SCRA 251 - G.R. No. L-24332 - January 31, 1978Ma AleNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress Assembled:: Further Amended To Read As FollowsDocument48 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress Assembled:: Further Amended To Read As FollowsmnyngNo ratings yet

- Sales MKTG NonongDocument3 pagesSales MKTG NonongmnyngNo ratings yet

- G.R. No. L-36770 November 4, 1932 LUIS W. DISON, Plaintiff-Appellant, JUAN POSADAS, JR., Collector of Internal Revenue, Defendant-AppellantDocument21 pagesG.R. No. L-36770 November 4, 1932 LUIS W. DISON, Plaintiff-Appellant, JUAN POSADAS, JR., Collector of Internal Revenue, Defendant-AppellantmnyngNo ratings yet

- LiwanagDocument1 pageLiwanagmnyngNo ratings yet

- Work EthicsDocument14 pagesWork EthicsArshad Mohd100% (1)

- Seeing The State Governance and Governmentality in India - BOOKDocument335 pagesSeeing The State Governance and Governmentality in India - BOOKSuresh KumarNo ratings yet

- LOCAL GOVERNANCE: An Inspiring Journey Into The FutureDocument143 pagesLOCAL GOVERNANCE: An Inspiring Journey Into The FutureChin Ket TolaNo ratings yet

- Civics CPT AnswersDocument7 pagesCivics CPT Answersbookworm2923No ratings yet

- CGDocument6 pagesCGShubhankar ThakurNo ratings yet

- 2005 09 05 - DR1Document1 page2005 09 05 - DR1Zach EdwardsNo ratings yet

- Ombudsman Seeks COA Help in Graft CaseDocument2 pagesOmbudsman Seeks COA Help in Graft CaseManuel MejoradaNo ratings yet

- Adolf Hitler 2Document6 pagesAdolf Hitler 2Muhammad Usman GhaniNo ratings yet

- Elizabeth Wilson, Individually and As Mother and Next Friend of Ailsa Debold v. Bradlees of New England, Inc., 96 F.3d 552, 1st Cir. (1996)Document12 pagesElizabeth Wilson, Individually and As Mother and Next Friend of Ailsa Debold v. Bradlees of New England, Inc., 96 F.3d 552, 1st Cir. (1996)Scribd Government DocsNo ratings yet

- National Security Policy, 2016Document55 pagesNational Security Policy, 2016LAVI TYAGINo ratings yet

- Macario SakayDocument3 pagesMacario Sakaymaria glayza corcueraNo ratings yet

- Sarah Birch - The Evolution of Electoral Integrity in New Democracies and Electoral Authoritarian RegimesDocument30 pagesSarah Birch - The Evolution of Electoral Integrity in New Democracies and Electoral Authoritarian RegimesHector MillanNo ratings yet

- Participation of Women French RevolutionDocument4 pagesParticipation of Women French RevolutionNahar SinghNo ratings yet

- FIA Assitant Director Batch 01 PaperDocument109 pagesFIA Assitant Director Batch 01 PaperAzan AliNo ratings yet

- PMG Zondo ReportDocument24 pagesPMG Zondo ReportjanetNo ratings yet

- Mavery Shye Sumbalan - Math 1 Module 2Q W2Document10 pagesMavery Shye Sumbalan - Math 1 Module 2Q W2Pidol MawileNo ratings yet

- Elpidio QuirinoDocument14 pagesElpidio Quirinosassymhine0% (1)

- Clarification Regarding 1. NOC and 2. Single Candidate To An Open Advertisement.Document1 pageClarification Regarding 1. NOC and 2. Single Candidate To An Open Advertisement.kanchankonwarNo ratings yet

- Independence For The Philippine IslandsDocument503 pagesIndependence For The Philippine IslandsJOHN PATRICK BERNARDINONo ratings yet

- Republic v. Holy TrinityDocument14 pagesRepublic v. Holy TrinityReal TaberneroNo ratings yet

- No Nim Nama Mahasiswa KetDocument5 pagesNo Nim Nama Mahasiswa KetMuhammad ZalilNo ratings yet