You might also like

- Real Estate AppraisalDocument2 pagesReal Estate Appraisalbekzod100% (1)

- Valuation of Real Estate (NIREM) 2nd Autust 2013Document69 pagesValuation of Real Estate (NIREM) 2nd Autust 2013Michael Ward0% (1)

- Commercial Appraisal OverviewDocument61 pagesCommercial Appraisal OverviewahmedNo ratings yet

- Real Estate Market AnalysisDocument48 pagesReal Estate Market AnalysisMila Agnas Silaba50% (2)

- Real estate appraisal formulas guideDocument4 pagesReal estate appraisal formulas guideMichelleOgatis83% (6)

- Guide To Real Property AppraisalDocument74 pagesGuide To Real Property AppraisalFrancisco Braganza100% (2)

- 5 Methods of ValuationDocument14 pages5 Methods of Valuationmennakhla100% (1)

- Appraisal Report WritingDocument3 pagesAppraisal Report WritingLGNo ratings yet

- Real Estate Appraiser Exam ReviewerDocument224 pagesReal Estate Appraiser Exam ReviewerJoey Lamban100% (6)

- 3 Valuation of Lease InterestsDocument23 pages3 Valuation of Lease InterestsPinoy Doto Best DotoNo ratings yet

- Valuation Methods for Real EstateDocument16 pagesValuation Methods for Real EstateKishor AhirNo ratings yet

- Market AnalysisDocument35 pagesMarket AnalysisbtittyNo ratings yet

- Real Estate Financial Modeling Training BrochureDocument21 pagesReal Estate Financial Modeling Training Brochurebkirschrefm50% (6)

- 5 AppraisalProcess MBC2015 PDFDocument70 pages5 AppraisalProcess MBC2015 PDFRoy John MalaluanNo ratings yet

- Appraisal Feasibility Study Ethics Business Valuation ConsultancyFrom EverandAppraisal Feasibility Study Ethics Business Valuation ConsultancyNo ratings yet

- 03 - Real Estate FinanceDocument513 pages03 - Real Estate FinanceFederica Rossini100% (2)

- Real Estate Valuation FactorsDocument52 pagesReal Estate Valuation FactorsRamesh KumarNo ratings yet

- Going Concern Valuation: For Real Estate Appraisers, Lenders, Assessors, and Eminent DomainFrom EverandGoing Concern Valuation: For Real Estate Appraisers, Lenders, Assessors, and Eminent DomainNo ratings yet

- Real Estate Investment AnalysisDocument67 pagesReal Estate Investment AnalysisRheneir MoraNo ratings yet

- Comprehensive Reviewer On AppraiserDocument15 pagesComprehensive Reviewer On AppraiserBelteshazzarL.CabacangNo ratings yet

- Table of Content For Rena's Market Analysis For Real EstateDocument11 pagesTable of Content For Rena's Market Analysis For Real Estatetashapa100% (1)

- Real Estate Valuation SeminarDocument96 pagesReal Estate Valuation SeminarSoftkiller67% (3)

- Valuation of Lease InterestsDocument30 pagesValuation of Lease InterestsRossvelt DucusinNo ratings yet

- Commercial Real Estate Case StudyDocument2 pagesCommercial Real Estate Case StudyKirk SummaTime Henry100% (1)

- Susquehanna Art Museum Building AppraisalDocument47 pagesSusquehanna Art Museum Building AppraisalPennLiveNo ratings yet

- Chapter 6-Income ApproachDocument37 pagesChapter 6-Income ApproachHosnii QamarNo ratings yet

- Real Estate Investment Analysis GuideDocument28 pagesReal Estate Investment Analysis GuideJ Ann ColipanoNo ratings yet

- Income ApproachDocument9 pagesIncome ApproachRoselle AbuelNo ratings yet

- Highest & Best Use of LandDocument21 pagesHighest & Best Use of LandarkiTOM18No ratings yet

- Appraisal Lecture HandoutDocument6 pagesAppraisal Lecture Handoutcharo calipayNo ratings yet

- 7 - Market ApproachDocument22 pages7 - Market ApproachThresia Navarro LadicaNo ratings yet

- Glossary of Real Estate TermsDocument5 pagesGlossary of Real Estate Termsskkarim90No ratings yet

- Cost ApproachDocument43 pagesCost ApproachMarites BalmasNo ratings yet

- Essentials of Real Estate FinanceDocument46 pagesEssentials of Real Estate FinanceJune AlapaNo ratings yet

- Capitalization RateDocument10 pagesCapitalization RateAndi Eka IftitahNo ratings yet

- Highest & Best Use: Basic Concepts: Stephen F. Fanning Mai, Cre, AicpDocument53 pagesHighest & Best Use: Basic Concepts: Stephen F. Fanning Mai, Cre, Aicpfrank100% (1)

- Introduction To Real Estate Valuation: Accelerating SuccessDocument54 pagesIntroduction To Real Estate Valuation: Accelerating SuccessJoseph J. AssafNo ratings yet

- Lectu Re 4. Land Valuation TechniquesDocument10 pagesLectu Re 4. Land Valuation TechniquesPeter Jean-jacques100% (1)

- Real Estate Valuation MethodsDocument29 pagesReal Estate Valuation MethodsMichael Jefferson100% (1)

- Highest and Best Use Problems in Market ValueDocument3 pagesHighest and Best Use Problems in Market Valuedpkkd100% (1)

- Reits101 AnIntroductionToRealEstate enDocument8 pagesReits101 AnIntroductionToRealEstate enGiovanni DustinNo ratings yet

- Final Valuation Report - DMI - FEB 2014Document33 pagesFinal Valuation Report - DMI - FEB 2014Soumi DasNo ratings yet

- Real Property Valuation Methods & TechniquesDocument7 pagesReal Property Valuation Methods & TechniquesLavanya LakshmiNo ratings yet

- Real Estate Appraisal A Review of Valuation Methods Vassilis AssimakopoulosDocument25 pagesReal Estate Appraisal A Review of Valuation Methods Vassilis AssimakopoulosBianca SferleNo ratings yet

- Guidelines For Real Estate Research and Case Study Analysis: January 2016Document129 pagesGuidelines For Real Estate Research and Case Study Analysis: January 2016dzun nurwinasNo ratings yet

- Buy and Optimize: A Guide to Acquiring and Owning Commercial PropertyFrom EverandBuy and Optimize: A Guide to Acquiring and Owning Commercial PropertyNo ratings yet

- Key ANS. Book4.4 Valuation and Appraisal RDL 55q 10p 2014Document11 pagesKey ANS. Book4.4 Valuation and Appraisal RDL 55q 10p 2014Noel RemolacioNo ratings yet

- Principles of Investment ValuationDocument38 pagesPrinciples of Investment ValuationSherineLiewNo ratings yet

- Basic Appraisal For Real Estate BrokerDocument107 pagesBasic Appraisal For Real Estate Brokerjames cruzNo ratings yet

- Real Property Appraisal PrinciplesDocument42 pagesReal Property Appraisal Principlesrrpenolio100% (1)

- Real Estate Market Analysis: Trends, Methods, and Information Sources, Third EditionFrom EverandReal Estate Market Analysis: Trends, Methods, and Information Sources, Third EditionRating: 3 out of 5 stars3/5 (1)

- Philippine real estate appraisal seminar conceptsDocument9 pagesPhilippine real estate appraisal seminar conceptsDiwaNo ratings yet

- Real Estate Mathematics Sample Problems (Ref: 0505) : I. Perimeter Fencing ProblemDocument4 pagesReal Estate Mathematics Sample Problems (Ref: 0505) : I. Perimeter Fencing ProblemGeorge Poligratis RicoNo ratings yet

- Basic Real Estate Appraisal Lecture Outline For Chapter 14Document24 pagesBasic Real Estate Appraisal Lecture Outline For Chapter 14Lovely Rose Ducusin100% (1)

- Real Estate Mathematics 2019Document47 pagesReal Estate Mathematics 2019soraya7560No ratings yet

- June 6 Review Exam For Module 4Document10 pagesJune 6 Review Exam For Module 4Roger ChivasNo ratings yet

- Slum Rehablitiaion ReportDocument65 pagesSlum Rehablitiaion Reportshivpreetsandhu100% (2)

- ICT DevelopmentDocument44 pagesICT DevelopmentshivpreetsandhuNo ratings yet

- The Time Value of MoneyDocument26 pagesThe Time Value of MoneyshivpreetsandhuNo ratings yet

- Slum Rehabilitation Schemes: 33.10 SchemeDocument5 pagesSlum Rehabilitation Schemes: 33.10 Schemeshivpreetsandhu100% (1)

- NGN Û Next Generation Network - Shivpreet, AbhijeevDocument29 pagesNGN Û Next Generation Network - Shivpreet, AbhijeevshivpreetsandhuNo ratings yet

- Exploring Real Estate InvestmentsDocument18 pagesExploring Real Estate InvestmentssengtohNo ratings yet

- Re 4Document10 pagesRe 4shivpreetsandhuNo ratings yet

- Sale Leaseback & MortgageDocument30 pagesSale Leaseback & MortgageshivpreetsandhuNo ratings yet

- Real EstateDocument25 pagesReal Estateshivpreetsandhu100% (1)

- Housing For The Poor in IndiaDocument16 pagesHousing For The Poor in IndiashivpreetsandhuNo ratings yet

- Re 1Document6 pagesRe 1shivpreetsandhuNo ratings yet

- Mergers & Acquisitions in Telecom IndustryDocument26 pagesMergers & Acquisitions in Telecom IndustryshivpreetsandhuNo ratings yet

- Real Estate Cycles What Is A Business Cycle?Document5 pagesReal Estate Cycles What Is A Business Cycle?shivpreetsandhuNo ratings yet

- FAR PresentationDocument29 pagesFAR PresentationshivpreetsandhuNo ratings yet

- Tower Infra2003Document30 pagesTower Infra2003shivpreetsandhuNo ratings yet

- Remote Infrastructure Monitoring & MGTDocument29 pagesRemote Infrastructure Monitoring & MGTshivpreetsandhuNo ratings yet

- Is It Better To Deploy 3GDocument9 pagesIs It Better To Deploy 3GshivpreetsandhuNo ratings yet

- Market Trends QualityDocument21 pagesMarket Trends QualityshivpreetsandhuNo ratings yet

- ISMSDocument23 pagesISMSshivpreetsandhu100% (1)

- Information Technology InfrastructureDocument29 pagesInformation Technology InfrastructureshivpreetsandhuNo ratings yet

- NOC and SOCDocument19 pagesNOC and SOCshivpreetsandhuNo ratings yet

- LTEDocument36 pagesLTEshivpreetsandhuNo ratings yet

- Indian TelecomDocument38 pagesIndian TelecomshivpreetsandhuNo ratings yet

- In DOMAIN Registration DerDocument20 pagesIn DOMAIN Registration DershivpreetsandhuNo ratings yet

- ICT DevelopmentDocument49 pagesICT DevelopmentshivpreetsandhuNo ratings yet

- ICTDocument21 pagesICTshivpreetsandhuNo ratings yet

- ICITM Relation To Service SupportDocument25 pagesICITM Relation To Service SupportshivpreetsandhuNo ratings yet

- GSM CDMA Network & Broadband Û India RoadmapDocument17 pagesGSM CDMA Network & Broadband Û India RoadmapshivpreetsandhuNo ratings yet

- Guidelines Related To enDocument28 pagesGuidelines Related To enshivpreetsandhuNo ratings yet

- Amundi Equity Global Disruptive Opportunities - UsdDocument2 pagesAmundi Equity Global Disruptive Opportunities - UsdEng Hau QuaNo ratings yet

- Multiple Projects & Constraints: Ranking, Mathematical Programming ApproachesDocument11 pagesMultiple Projects & Constraints: Ranking, Mathematical Programming ApproachesVinayGolchha100% (1)

- Jain BBA Financial Management Practice PaperDocument2 pagesJain BBA Financial Management Practice PaperRavichandraNo ratings yet

- Narayana Health: The Initial Ipo DecisionDocument9 pagesNarayana Health: The Initial Ipo DecisionKANVI KAUSHIKNo ratings yet

- The Impact of Working Capital Management On The Performance of Food and Beverages IndustryDocument6 pagesThe Impact of Working Capital Management On The Performance of Food and Beverages IndustrySaheed NureinNo ratings yet

- R12 Org Blueprint for Separate Centric/BPI OUDocument6 pagesR12 Org Blueprint for Separate Centric/BPI OUqkhan2000No ratings yet

- The Biggest Fund Investors in Private EquityDocument7 pagesThe Biggest Fund Investors in Private EquityDavid KeresztesNo ratings yet

- NCFM Module On Mutual FundsDocument123 pagesNCFM Module On Mutual Fundsanjusawlani86No ratings yet

- Week 4 Topic 1 Aqad and Sources of FundsDocument41 pagesWeek 4 Topic 1 Aqad and Sources of Funds2 Ashlih Al TsabatNo ratings yet

- Exchange Ratio - Problems N SolutionsDocument26 pagesExchange Ratio - Problems N SolutionsBrowse Purpose82% (17)

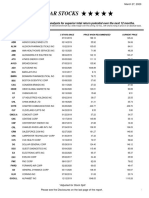

- Five Star StocksDocument5 pagesFive Star StocksJeff SturgeonNo ratings yet

- Financial Management Chapter 02 IM 10th EdDocument21 pagesFinancial Management Chapter 02 IM 10th EdDr Rushen SinghNo ratings yet

- Fin Mar Script TineDocument3 pagesFin Mar Script TineChristine RepuldaNo ratings yet

- Awareness Among The Traders About The Settlement of Online TradingDocument13 pagesAwareness Among The Traders About The Settlement of Online TradingElson Antony PaulNo ratings yet

- Apollo HospitalsDocument18 pagesApollo HospitalsvishalNo ratings yet

- IRM Chapter 2 Concept ReviewsDocument6 pagesIRM Chapter 2 Concept ReviewsJustine Belle FryorNo ratings yet

- Auditing ElementsDocument25 pagesAuditing ElementsBWAMBALE SALVERI MUZANANo ratings yet

- Global Reinsurance Highlights 2018Document88 pagesGlobal Reinsurance Highlights 2018sumanT9No ratings yet

- Annual Report Project On Muthoot Finance LTDDocument39 pagesAnnual Report Project On Muthoot Finance LTDAnu ArjaNo ratings yet

- 1033. ტურიზმის-მარკეტინგი-სოფო-თევდორაძეDocument120 pages1033. ტურიზმის-მარკეტინგი-სოფო-თევდორაძეAnton SinatashviliNo ratings yet

- Gold - Love N Fear TradesDocument62 pagesGold - Love N Fear TradesgautamswamiNo ratings yet

- Business Combination - TheoriesDocument11 pagesBusiness Combination - TheoriesMILLARE, Teddy Glo B.No ratings yet

- D) Both B and C: Balance of Payments Total Weightage-6 MarksDocument9 pagesD) Both B and C: Balance of Payments Total Weightage-6 MarksShreya PushkarnaNo ratings yet

- Accounting For Legal Reorganizations and Liquidations: Multiple Choice QuestionsDocument121 pagesAccounting For Legal Reorganizations and Liquidations: Multiple Choice Questionsjana ayoubNo ratings yet

- Tugas Manajemen KeuanganDocument3 pagesTugas Manajemen KeuanganmunawarchalilNo ratings yet

- Practice For Quiz #3 Solutions For StudentsDocument10 pagesPractice For Quiz #3 Solutions For Studentssylstria.mcNo ratings yet

- SCDL Financial Management Sample QuestionsDocument8 pagesSCDL Financial Management Sample QuestionsketanNo ratings yet

- PT Semen Indonesia q3 2022 - FinalDocument112 pagesPT Semen Indonesia q3 2022 - FinalHaris MaulanaNo ratings yet

- Bus 305 AOCDocument4 pagesBus 305 AOCOyeniyi farukNo ratings yet

- Rayner Teo - Notes On Ultimate Guide To Price Action Trading 18.12.21Document2 pagesRayner Teo - Notes On Ultimate Guide To Price Action Trading 18.12.21Joy Cheung100% (1)