You might also like

- Tilted Justice: First Came the Flood, Then Came the Lawyers.From EverandTilted Justice: First Came the Flood, Then Came the Lawyers.No ratings yet

- The Philippine Law Journal and The Development of Law by Antonio CarpioDocument2 pagesThe Philippine Law Journal and The Development of Law by Antonio Carpiolocusstandi84No ratings yet

- Fraport II Vs PHDocument15 pagesFraport II Vs PHCharm Agripa100% (1)

- Administrative Circular No. 12-94-Amendments To R114-BailDocument4 pagesAdministrative Circular No. 12-94-Amendments To R114-BailAngela Canares100% (1)

- Court Case Loan DisputeDocument7 pagesCourt Case Loan DisputeZy AquilizanNo ratings yet

- Gonzales vs. Hechanova, G.R. No. L-21897, October 22, 1963Document10 pagesGonzales vs. Hechanova, G.R. No. L-21897, October 22, 1963Jelena SebastianNo ratings yet

- Carlo's Judicial and Legal EthicsDocument13 pagesCarlo's Judicial and Legal EthicsCarlo MagsilaoNo ratings yet

- People Vs PurisimaDocument4 pagesPeople Vs PurisimaAname Barredo0% (1)

- Court Dismissal of Construction Collection CaseDocument3 pagesCourt Dismissal of Construction Collection CaseSuju BudolNo ratings yet

- Assignment 2 Answer KeyDocument2 pagesAssignment 2 Answer KeyAbdulakbar Ganzon BrigoleNo ratings yet

- The Integrated Bar of the Philippines: What is IBPDocument31 pagesThe Integrated Bar of the Philippines: What is IBPRubz JeanNo ratings yet

- Affidavit of Release On Own RecognizanceDocument3 pagesAffidavit of Release On Own RecognizanceBai Alefha Hannah Musa-AbubacarNo ratings yet

- Part I. 2-Point QuestionsDocument5 pagesPart I. 2-Point QuestionsLily MondaragonNo ratings yet

- Bill of Rights LectureDocument3 pagesBill of Rights LectureAnonymous lYBiiLhNo ratings yet

- Guarantor rights and obligations between debtor and creditorDocument10 pagesGuarantor rights and obligations between debtor and creditormichaelargabiosoNo ratings yet

- BDO-2019-Sustainability Report PDFDocument72 pagesBDO-2019-Sustainability Report PDFJohn Michael Dela CruzNo ratings yet

- Legal SeparationDocument33 pagesLegal SeparationAngel UrbanoNo ratings yet

- Term Paper - AMLA and Banking Laws - Jason Oliver SunDocument6 pagesTerm Paper - AMLA and Banking Laws - Jason Oliver SunJason SunNo ratings yet

- DOJ Memo On Tribal Pot PoliciesDocument3 pagesDOJ Memo On Tribal Pot Policiesstevennelson10100% (1)

- White Marketing vs. Grandwood Furniture, 23 November 2016Document6 pagesWhite Marketing vs. Grandwood Furniture, 23 November 2016doora keysNo ratings yet

- Banking Laws Course Syllabus AY20-21Document3 pagesBanking Laws Course Syllabus AY20-21Paolo SueltoNo ratings yet

- Quiz No.1 - Ryan Paul Aquino - SN22-00258Document1 pageQuiz No.1 - Ryan Paul Aquino - SN22-00258RPSA CPANo ratings yet

- Income Taxation Outline and CasesDocument7 pagesIncome Taxation Outline and CasesChicklet ArponNo ratings yet

- Should We Go BeyondDocument2 pagesShould We Go Beyondpriam gabriel d salidagaNo ratings yet

- State Immunity Doctrine Applied to Rice AgencyDocument4 pagesState Immunity Doctrine Applied to Rice Agencyflordelei hocateNo ratings yet

- MemorandumDocument3 pagesMemorandumBurn-Cindy AbadNo ratings yet

- The Honorable Office of The Ombudsman v. Leovigildo Delos Reyes, JRDocument12 pagesThe Honorable Office of The Ombudsman v. Leovigildo Delos Reyes, JRRAINBOW AVALANCHENo ratings yet

- Rodriguez vs. Martinez, 5 Phil. 67, No. 1913 September 29, 1905 (Alvarez)Document2 pagesRodriguez vs. Martinez, 5 Phil. 67, No. 1913 September 29, 1905 (Alvarez)Koolen AlvarezNo ratings yet

- De La Salle UniversityDocument4 pagesDe La Salle UniversityRonn Robby RosalesNo ratings yet

- Ong Chua V. Edward Carr Et AlDocument4 pagesOng Chua V. Edward Carr Et AlrobbyNo ratings yet

- Supreme Court Holds President Personally Liable for Debts of Non-Existent CorporationDocument6 pagesSupreme Court Holds President Personally Liable for Debts of Non-Existent Corporationmarc bantugNo ratings yet

- Sample ComplaintDocument32 pagesSample ComplaintericsuterNo ratings yet

- PEOPLE Vs MARTI, GR 81561 Jan.18.1991 - Case Digest - CantoriaDocument2 pagesPEOPLE Vs MARTI, GR 81561 Jan.18.1991 - Case Digest - CantoriaGianna CantoriaNo ratings yet

- Carale vs. AbarintosDocument13 pagesCarale vs. AbarintosRustom IbañezNo ratings yet

- Civ-Pro Avena Q&A ReviewerDocument2 pagesCiv-Pro Avena Q&A Reviewercmv mendozaNo ratings yet

- Chapter 3 Lesson 2 Rights of PDLDocument13 pagesChapter 3 Lesson 2 Rights of PDLKent Denyl ManlupigNo ratings yet

- Campos v. People G.R. No. 187401Document4 pagesCampos v. People G.R. No. 187401fgNo ratings yet

- REGALA VS SANDIGANBAYAN Version 4Document2 pagesREGALA VS SANDIGANBAYAN Version 4roberto valenzuelaNo ratings yet

- 2022 Banking Case Digest FinalDocument18 pages2022 Banking Case Digest FinalJem PagantianNo ratings yet

- Dear PAODocument15 pagesDear PAOCharisse Dianne PanayNo ratings yet

- A.M. 00-2-01 SC Legal FeesDocument10 pagesA.M. 00-2-01 SC Legal FeesattyrichiereyNo ratings yet

- ComplaintDocument10 pagesComplaintJu BalajadiaNo ratings yet

- UST GN 2011 Legal and Judicial Ethics Proper Index 4Document130 pagesUST GN 2011 Legal and Judicial Ethics Proper Index 4Timmy HaliliNo ratings yet

- Erlaine Vanessa D. Lumanog Constitutional Law 2 - Atty. MedinaDocument23 pagesErlaine Vanessa D. Lumanog Constitutional Law 2 - Atty. MedinaAndrea Gural De GuzmanNo ratings yet

- Legal Research For First QuizDocument8 pagesLegal Research For First QuizJazireeNo ratings yet

- Compilation For ConstiDocument53 pagesCompilation For ConstiAdri MillerNo ratings yet

- Enforcing a US Court JudgmentDocument16 pagesEnforcing a US Court JudgmentAubrey AquinoNo ratings yet

- PPSAS 26 Impairment of Cash Generating AssetsDocument3 pagesPPSAS 26 Impairment of Cash Generating AssetsAr LineNo ratings yet

- Equitable Interest Rate. All The Foregoing Notwithstanding, We Are of The Opinion ThatDocument2 pagesEquitable Interest Rate. All The Foregoing Notwithstanding, We Are of The Opinion ThatBoy Omar Garangan DatudaculaNo ratings yet

- Lim Vs PeopleDocument10 pagesLim Vs PeopleDaryl Noel TejanoNo ratings yet

- Far East vs. CaDocument5 pagesFar East vs. CaLenPalatanNo ratings yet

- PUP Obligation and Contracts Lesson 2 1Document89 pagesPUP Obligation and Contracts Lesson 2 1Jerome TimolaNo ratings yet

- Quiz No.6 - Ryan Paul Aquino - SN22-00258Document2 pagesQuiz No.6 - Ryan Paul Aquino - SN22-00258RPSA CPANo ratings yet

- Atty misconduct caseDocument6 pagesAtty misconduct caseandangNo ratings yet

- Banco de Oro Vs Ypil, GR 212024, Oct. 12, 2020Document14 pagesBanco de Oro Vs Ypil, GR 212024, Oct. 12, 2020dee zoeNo ratings yet

- PLJ Volume 51 Number 1 & 2 - 05 - Pelagio T. Ricalde - Mr. Chief Justice Conception On Judicial Review P. 103-123Document21 pagesPLJ Volume 51 Number 1 & 2 - 05 - Pelagio T. Ricalde - Mr. Chief Justice Conception On Judicial Review P. 103-123Christine ErnoNo ratings yet

- War crimes and crimes against humanity in the Rome Statute of the International Criminal CourtFrom EverandWar crimes and crimes against humanity in the Rome Statute of the International Criminal CourtNo ratings yet

- General Banking Law Outline on RA 8791Document28 pagesGeneral Banking Law Outline on RA 8791JM EnguitoNo ratings yet

- Banking Law, Central Bank Act, SRC, Foreign Investment, Letters of CreditDocument45 pagesBanking Law, Central Bank Act, SRC, Foreign Investment, Letters of Creditflordeluna ayingNo ratings yet

- Englih 4 - Argumentation and DebateDocument1 pageEnglih 4 - Argumentation and Debatejade123_129No ratings yet

- For Envelope CoverDocument1 pageFor Envelope Coverjade123_129No ratings yet

- Sole Proprietorship: Corporation Code RegisteredDocument1 pageSole Proprietorship: Corporation Code Registeredjade123_129No ratings yet

- ADocument1 pageAjade123_129No ratings yet

- 5-Manual For Lawyers and Parties Rules 22 and 24Document22 pages5-Manual For Lawyers and Parties Rules 22 and 24Stephen Jorge Abellana EsparagozaNo ratings yet

- The Secret ExtractDocument11 pagesThe Secret ExtractGulam mustafaNo ratings yet

- Affidavit of Loss I,, of Legal Age, Single, Filipino Citizen and A Resident of Digos CityDocument1 pageAffidavit of Loss I,, of Legal Age, Single, Filipino Citizen and A Resident of Digos Cityjade123_129No ratings yet

- Affidavit of Undertakings for MotorcycleDocument1 pageAffidavit of Undertakings for Motorcyclejade123_129No ratings yet

- Acknowledgment ReceiptDocument1 pageAcknowledgment Receiptjade123_129No ratings yet

- Jaai Oath of Office Aug 6, 2018Document1 pageJaai Oath of Office Aug 6, 2018jade123_129No ratings yet

- Technical Writing ExplainedDocument9 pagesTechnical Writing Explainedjade123_129No ratings yet

- For Envelope CoverDocument1 pageFor Envelope Coverjade123_129No ratings yet

- Legal DocumentDocument2 pagesLegal Documentjade123_129No ratings yet

- Chain of Custody and Dna EvidenceDocument5 pagesChain of Custody and Dna Evidencejade123_129No ratings yet

- 1st Jose Maria College Alumni Reunion 2003-2013Document1 page1st Jose Maria College Alumni Reunion 2003-2013jade123_129No ratings yet

- Criminal Law I Syllabus Jose Maria CollegeDocument2 pagesCriminal Law I Syllabus Jose Maria Collegejade123_129No ratings yet

- Gervacio: (Nora Chang Transcriptions)Document2 pagesGervacio: (Nora Chang Transcriptions)jade123_129No ratings yet

- Affidavit of Loss Apple Mae ShiromaDocument1 pageAffidavit of Loss Apple Mae Shiromajade123_129No ratings yet

- Correct Name AffidavitDocument1 pageCorrect Name Affidavitjade123_129No ratings yet

- Henry G Funda, JR - David Yu Kimteng Vs Atty Walter YoungDocument4 pagesHenry G Funda, JR - David Yu Kimteng Vs Atty Walter Youngjade123_129100% (3)

- Final Grouping Legal PhilosophyDocument3 pagesFinal Grouping Legal Philosophyjade123_129No ratings yet

- Documentary Requirements For Franchise ApplicationDocument3 pagesDocumentary Requirements For Franchise Applicationjade123_129No ratings yet

- Kinds of SharesDocument1 pageKinds of Sharesjade123_129No ratings yet

- Legal Philosophy ReportingDocument1 pageLegal Philosophy Reportingjade123_129No ratings yet

- Certification of Number of Foreign EmployeesDocument1 pageCertification of Number of Foreign Employeesjade123_129No ratings yet

- Certification of Number of Foreign EmployeesDocument1 pageCertification of Number of Foreign Employeesjade123_129No ratings yet

- English 2 AttendanceDocument2 pagesEnglish 2 Attendancejade123_129No ratings yet

- Continuous TrialDocument5 pagesContinuous Trialjade123_129No ratings yet

- Moa - Social WorkDocument3 pagesMoa - Social Workjade123_129No ratings yet

- Canada Large NotepadsDocument3 pagesCanada Large Notepadsjade123_129No ratings yet

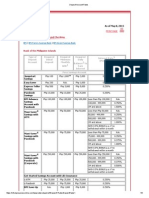

- BPI Deposit Account RatesDocument5 pagesBPI Deposit Account Ratesparekoy1014No ratings yet

- CBSE Class 10 Social Science Chapter-3 Money and Credit NotesDocument4 pagesCBSE Class 10 Social Science Chapter-3 Money and Credit NotesVishrut Shahi100% (1)

- Jan 192014 Dos 01 eDocument11 pagesJan 192014 Dos 01 erakhalbanglaNo ratings yet

- Subrata Dhara Paytm StatementDocument2 pagesSubrata Dhara Paytm StatementShúbhám ChoúnipurgéNo ratings yet

- Consolidated Reports of Condition and Income For A Bank With Domestic Offices Only and Total Assets Less Than $5 Billion - FFIEC 051Document55 pagesConsolidated Reports of Condition and Income For A Bank With Domestic Offices Only and Total Assets Less Than $5 Billion - FFIEC 051billNo ratings yet

- Fintech and Banking. Friends or Foes?: University of MilanDocument38 pagesFintech and Banking. Friends or Foes?: University of MilanMinh QuangNo ratings yet

- Industrial FinanceDocument11 pagesIndustrial Financedesaijpr90% (10)

- Pak Enings HTDocument15 pagesPak Enings HTVincent SampianoNo ratings yet

- E Cash Payment SystemDocument29 pagesE Cash Payment Systemhareesh64kumar100% (2)

- Required Forms For SCSSDocument16 pagesRequired Forms For SCSSmurugeshlpNo ratings yet

- Concept of Commercial Banks of Nepa1Document8 pagesConcept of Commercial Banks of Nepa1vanvunNo ratings yet

- PDF To WordDocument93 pagesPDF To WordRenu SharmaNo ratings yet

- EXIM Finance Unit IIDocument11 pagesEXIM Finance Unit IIloganathanNo ratings yet

- Foreign Currency Deposits: R.A 6426, SEC 8Document38 pagesForeign Currency Deposits: R.A 6426, SEC 8Israel BandonillNo ratings yet

- Central Bank exempt from paying interest during suspensionDocument3 pagesCentral Bank exempt from paying interest during suspensionAntonio Rebosa0% (1)

- Benchmarking Top Arab Banks' Efficiency Through Efficient Frontier AnalysisDocument25 pagesBenchmarking Top Arab Banks' Efficiency Through Efficient Frontier AnalysisDavid Adeabah OsafoNo ratings yet

- Money and BankingDocument13 pagesMoney and BankingVirencarpediem0% (1)

- The Functions of Bangladesh BankDocument10 pagesThe Functions of Bangladesh BankMd. Rakibul Hasan Rony93% (14)

- Currency Chest RavishDocument14 pagesCurrency Chest Ravishravish419No ratings yet

- Financial SectorDocument13 pagesFinancial Sectormadiha113No ratings yet

- Salient Features of Policy For Engagement of Recovery AgenciesDocument17 pagesSalient Features of Policy For Engagement of Recovery Agenciesashaorissa1997No ratings yet

- 26as Ay 21-22Document4 pages26as Ay 21-22Madhu MohanNo ratings yet

- TSB Form 1Document2 pagesTSB Form 1EldhoThomasNo ratings yet

- Deposit Contract EssentialsDocument16 pagesDeposit Contract EssentialsCJ FaNo ratings yet

- BFSI Training Manual - PDF - 20230810 - 164502 - 0000Document50 pagesBFSI Training Manual - PDF - 20230810 - 164502 - 0000deepak643aNo ratings yet

- Functions of RBIDocument3 pagesFunctions of RBITarun BhatejaNo ratings yet

- Bank Reconciliation Program (Excel)Document17 pagesBank Reconciliation Program (Excel)Rupert Parsons100% (3)

- FIN380 Term PaperDocument37 pagesFIN380 Term Paperনাজমুস সাদাবNo ratings yet

- Exercise Week 2 - Cash and ReceivablesDocument4 pagesExercise Week 2 - Cash and Receivablesnatasha karyadiNo ratings yet

- WB Treasury RulesDocument498 pagesWB Treasury Rulesnandi_scr100% (1)