You might also like

- Ironridge Global IV, Ltd. Declaration of Brendan O'NeilDocument27 pagesIronridge Global IV, Ltd. Declaration of Brendan O'NeilIronridge Global PartnersNo ratings yet

- 6th Interim ReportDocument13 pages6th Interim ReportRaúl DiazNo ratings yet

- Attorneys For Midland Loan Services, Inc.: Declaration of Ronald F. Greenspan Page 1 of 13 F-283364Document37 pagesAttorneys For Midland Loan Services, Inc.: Declaration of Ronald F. Greenspan Page 1 of 13 F-283364Chapter 11 DocketsNo ratings yet

- 01 PCIBank Versus CADocument4 pages01 PCIBank Versus CAArahbellsNo ratings yet

- Count One (Subscribing To A False Tax Return) : 2016R00573/DAG/CMDocument9 pagesCount One (Subscribing To A False Tax Return) : 2016R00573/DAG/CMGMG EditorialNo ratings yet

- Toys R Us Debtors Motion For Entry of OrdersDocument124 pagesToys R Us Debtors Motion For Entry of OrdersStephen LoiaconiNo ratings yet

- 2018.10.24 (2115) Decl. of J. Slavek ISO of CVX's Mtn. To Hold Donziger in ContemptDocument22 pages2018.10.24 (2115) Decl. of J. Slavek ISO of CVX's Mtn. To Hold Donziger in ContemptMichaelKraussNo ratings yet

- United States Court of Appeals, Sixth CircuitDocument14 pagesUnited States Court of Appeals, Sixth CircuitScribd Government DocsNo ratings yet

- ToysRUs March 2018Document124 pagesToysRUs March 2018Ben SchultzNo ratings yet

- In the Matter of Seminole Park and Fairgrounds, Inc., Bankrupt. Robert Dyer, Trustee, Seminole Park and Fairgrounds, Inc. v. First National Bank at Orlando, Indenture Trustee, 502 F.2d 1011, 1st Cir. (1974)Document7 pagesIn the Matter of Seminole Park and Fairgrounds, Inc., Bankrupt. Robert Dyer, Trustee, Seminole Park and Fairgrounds, Inc. v. First National Bank at Orlando, Indenture Trustee, 502 F.2d 1011, 1st Cir. (1974)Scribd Government DocsNo ratings yet

- 10000000736Document94 pages10000000736Chapter 11 DocketsNo ratings yet

- A Corrected Message From The SIPA Trustee's Chief Counsel, David J. SheehanDocument2 pagesA Corrected Message From The SIPA Trustee's Chief Counsel, David J. SheehanInvestor ProtectionNo ratings yet

- USDC FLA WPB Spring Intervene Response To Motion June22Document43 pagesUSDC FLA WPB Spring Intervene Response To Motion June22JaniceWolkGrenadierNo ratings yet

- 10000003728Document32 pages10000003728Chapter 11 DocketsNo ratings yet

- Cta 2D CV 06202 A 2009apr14 AssDocument21 pagesCta 2D CV 06202 A 2009apr14 AssAlfonso LeeNo ratings yet

- Affidavit of ResCap C.F.O.Document101 pagesAffidavit of ResCap C.F.O.DealBook100% (1)

- Harbeck Responds To Letter From Cong. GarrettDocument28 pagesHarbeck Responds To Letter From Cong. GarrettIlene KentNo ratings yet

- The Merchants National Bank of Mobile, Plaintiff-Counter v. United States of America, Defendant-Counter, 878 F.2d 1382, 11th Cir. (1989)Document11 pagesThe Merchants National Bank of Mobile, Plaintiff-Counter v. United States of America, Defendant-Counter, 878 F.2d 1382, 11th Cir. (1989)Scribd Government DocsNo ratings yet

- PHILIPPINE COMMERCIAL INTERNATIONAL BANK (Formerly INSULAR BANK OF ASIA AND AMERICA), Petitioner, vs. COURT OF APPEALS and FORD PHILIPPINES, INC. and CITIBANK, N.A., Respondents.Document7 pagesPHILIPPINE COMMERCIAL INTERNATIONAL BANK (Formerly INSULAR BANK OF ASIA AND AMERICA), Petitioner, vs. COURT OF APPEALS and FORD PHILIPPINES, INC. and CITIBANK, N.A., Respondents.Karen PascalNo ratings yet

- Neral Banking LawsDocument5 pagesNeral Banking LawsBadronDimangadapNo ratings yet

- U.S. Trustee's Objection To Evercore Partners's G.M. FeesDocument17 pagesU.S. Trustee's Objection To Evercore Partners's G.M. FeesDealBook100% (3)

- Cordjllera Golf Club, LLC Dba The Club at CordilleraDocument5 pagesCordjllera Golf Club, LLC Dba The Club at CordilleraChapter 11 DocketsNo ratings yet

- Receivers Second Interim Report Regading Status of ReceivershipDocument26 pagesReceivers Second Interim Report Regading Status of ReceivershipcburnellNo ratings yet

- Fox Rothschild LLP Yann Geron Kathleen Aiello 100 Park Avenue, 15 Floor New York, New York 10017 (212) 878-7900Document27 pagesFox Rothschild LLP Yann Geron Kathleen Aiello 100 Park Avenue, 15 Floor New York, New York 10017 (212) 878-7900Chapter 11 DocketsNo ratings yet

- U.S. v. Keith Douglas Freeman IndictmentDocument11 pagesU.S. v. Keith Douglas Freeman IndictmentTed Flores100% (1)

- AICPA Released Questions REG 2015 DifficultDocument22 pagesAICPA Released Questions REG 2015 DifficultKhalil JacksonNo ratings yet

- Cases Involving Auditors' NegligenceDocument5 pagesCases Involving Auditors' NegligenceJaden EuNo ratings yet

- United States Court of Appeals, Fourth CircuitDocument8 pagesUnited States Court of Appeals, Fourth CircuitScribd Government DocsNo ratings yet

- Sample Forensic Audit 26045678Document15 pagesSample Forensic Audit 26045678KNOWLEDGE SOURCENo ratings yet

- Pacific Banking Corporation Employees Organization vs. Court of AppealsDocument18 pagesPacific Banking Corporation Employees Organization vs. Court of AppealsDianne May CruzNo ratings yet

- Counsel For Debtor and Debtor-in-Possession: United States Bankruptcy Court For The District of NevadaDocument16 pagesCounsel For Debtor and Debtor-in-Possession: United States Bankruptcy Court For The District of NevadajaxxstrawNo ratings yet

- PDIC vs Citibank and Bank of AmericaDocument10 pagesPDIC vs Citibank and Bank of AmericaJoyce KevienNo ratings yet

- G.R. No. 170290 - Philippine Deposit Insurance Corp. v. CitibankDocument9 pagesG.R. No. 170290 - Philippine Deposit Insurance Corp. v. CitibankAmielle CanilloNo ratings yet

- Risinger IndictDocument14 pagesRisinger Indictjmaglich1No ratings yet

- 10000004274Document43 pages10000004274Chapter 11 DocketsNo ratings yet

- Merger of Community Bank and Company, OFR Petition For Public HearingDocument346 pagesMerger of Community Bank and Company, OFR Petition For Public HearingNeil Gillespie0% (1)

- Biolsi V Jefferson Capital Systems LLC FDCPA Complaint Debt CollectionDocument8 pagesBiolsi V Jefferson Capital Systems LLC FDCPA Complaint Debt CollectionghostgripNo ratings yet

- Verified Statement of Multiple Representation: CompanyDocument3 pagesVerified Statement of Multiple Representation: CompanyChapter 11 DocketsNo ratings yet

- Westmont Bank v. InlandDocument3 pagesWestmont Bank v. InlandTricia SandovalNo ratings yet

- United States v. R. Peter Stanham, 11th Cir. (2010)Document44 pagesUnited States v. R. Peter Stanham, 11th Cir. (2010)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Eleventh CircuitDocument9 pagesUnited States Court of Appeals, Eleventh CircuitScribd Government DocsNo ratings yet

- PNB LIABLE FOR NEGLIGENCE; HIGHER STANDARD FOR BANKSDocument7 pagesPNB LIABLE FOR NEGLIGENCE; HIGHER STANDARD FOR BANKSCarlu YooNo ratings yet

- 0708 DisDocument17 pages0708 DisAlexShearNo ratings yet

- Philippine deposit insurance ruling on inter-branch fundsDocument12 pagesPhilippine deposit insurance ruling on inter-branch fundsjmarkgNo ratings yet

- MRS V JPMC Doc 272, Declaration Rick Ivie - Jan 22, 2018 Declaration Rick IvieDocument3 pagesMRS V JPMC Doc 272, Declaration Rick Ivie - Jan 22, 2018 Declaration Rick Ivielarry-612445No ratings yet

- United States Bankruptcy Court Southern District of New YorkDocument19 pagesUnited States Bankruptcy Court Southern District of New YorkTBP_Think_TankNo ratings yet

- No Hearing RequiredDocument27 pagesNo Hearing RequiredChapter 11 DocketsNo ratings yet

- Central European Distribution Corporation Wins Overwhelming Creditor Approval of Proposed Restructuring PlanDocument3 pagesCentral European Distribution Corporation Wins Overwhelming Creditor Approval of Proposed Restructuring PlanChapter 11 DocketsNo ratings yet

- United States Court of Appeals, Fourth CircuitDocument7 pagesUnited States Court of Appeals, Fourth CircuitScribd Government DocsNo ratings yet

- I T U S B C F T D O C: N HE Nited Tates Ankruptcy Ourt OR HE Istrict F OloradoDocument14 pagesI T U S B C F T D O C: N HE Nited Tates Ankruptcy Ourt OR HE Istrict F OloradoChapter 11 DocketsNo ratings yet

- Saintvil IndictmentDocument22 pagesSaintvil IndictmentNick SchwellenbachNo ratings yet

- Attorneys For Midland Loan Services, Inc.: Declaration of Ronald F. Greenspan Pagel Of3Document3 pagesAttorneys For Midland Loan Services, Inc.: Declaration of Ronald F. Greenspan Pagel Of3Chapter 11 DocketsNo ratings yet

- Suit Against Yellowstone PartnersDocument17 pagesSuit Against Yellowstone PartnersJeff RobinsonNo ratings yet

- NJ Forensic Analysis SampleDocument77 pagesNJ Forensic Analysis Sampleagold73No ratings yet

- Southern Bancorporation, Inc. v. Commissioner of Internal Revenue, 847 F.2d 131, 4th Cir. (1988)Document11 pagesSouthern Bancorporation, Inc. v. Commissioner of Internal Revenue, 847 F.2d 131, 4th Cir. (1988)Scribd Government DocsNo ratings yet

- Securities and Exchange Commission v. Bridge Premium Finance, Michael J. Turnock and William P. Sullivan IIDocument33 pagesSecurities and Exchange Commission v. Bridge Premium Finance, Michael J. Turnock and William P. Sullivan IIMichael_Lee_RobertsNo ratings yet

- ResCap KERP OpinionDocument22 pagesResCap KERP OpinionChapter 11 DocketsNo ratings yet

- Regulation A+ and Other Alternatives to a Traditional IPO: Financing Your Growth Business Following the JOBS ActFrom EverandRegulation A+ and Other Alternatives to a Traditional IPO: Financing Your Growth Business Following the JOBS ActNo ratings yet

- Whistleblowers: Incentives, Disincentives, and Protection StrategiesFrom EverandWhistleblowers: Incentives, Disincentives, and Protection StrategiesNo ratings yet

- Vermont Resort Skier Visits Winter 2017-18Document1 pageVermont Resort Skier Visits Winter 2017-18CloverWhithamNo ratings yet

- Sources of Population Change in Vermont Counties 2010-2017Document1 pageSources of Population Change in Vermont Counties 2010-2017CloverWhithamNo ratings yet

- Vermont Sales Tax: Retail Spending in Vermont and New HampshireDocument1 pageVermont Sales Tax: Retail Spending in Vermont and New HampshireCloverWhithamNo ratings yet

- Social Security Recipients in VermontDocument1 pageSocial Security Recipients in VermontCloverWhithamNo ratings yet

- Vermont Job Growth Estimates vs. RealityDocument1 pageVermont Job Growth Estimates vs. RealityCloverWhithamNo ratings yet

- Vermont and New England Per Capita Personal IncomeDocument1 pageVermont and New England Per Capita Personal IncomeCloverWhithamNo ratings yet

- Population Change in Great Burlington VT AreaDocument1 pagePopulation Change in Great Burlington VT AreaCloverWhithamNo ratings yet

- Vermont's Median AgeDocument1 pageVermont's Median AgeCloverWhithamNo ratings yet

- Housing Growth by Vermont County 2017Document1 pageHousing Growth by Vermont County 2017CloverWhithamNo ratings yet

- Vermont School EnrollmentsDocument1 pageVermont School EnrollmentsCloverWhithamNo ratings yet

- Vermont's Inflation Adjusted Gross Domestic ProductDocument1 pageVermont's Inflation Adjusted Gross Domestic ProductCloverWhithamNo ratings yet

- Median Family Income in VermontDocument1 pageMedian Family Income in VermontCloverWhithamNo ratings yet

- Births To 2017Document1 pageBirths To 2017CloverWhithamNo ratings yet

- Housing Affordability in VermontDocument1 pageHousing Affordability in VermontCloverWhithamNo ratings yet

- Vermont's NEAP Test Scores 2017Document1 pageVermont's NEAP Test Scores 2017CloverWhithamNo ratings yet

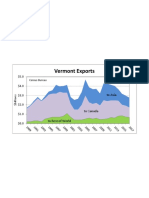

- Vermont Export Values 1981 To 2017Document1 pageVermont Export Values 1981 To 2017CloverWhithamNo ratings yet

- Vermont Births FromDocument1 pageVermont Births FromCloverWhithamNo ratings yet

- Vermont Labor Force and Payroll EmploymentDocument1 pageVermont Labor Force and Payroll EmploymentCloverWhithamNo ratings yet

- Housing Prices in VermontDocument1 pageHousing Prices in VermontCloverWhithamNo ratings yet

- Unemployment Insurance ClaimsDocument1 pageUnemployment Insurance ClaimsCloverWhithamNo ratings yet

- Electricity Rates by State, Top 10 and Bottom 10Document1 pageElectricity Rates by State, Top 10 and Bottom 10CloverWhithamNo ratings yet

- Vermont Education Spending Compared To U.S. AverageDocument1 pageVermont Education Spending Compared To U.S. AverageCloverWhithamNo ratings yet

- Outmigrants To Florida From VermontDocument1 pageOutmigrants To Florida From VermontCloverWhithamNo ratings yet

- Components of Vermont's Population Change Over TimeDocument1 pageComponents of Vermont's Population Change Over TimeCloverWhithamNo ratings yet

- Population Growth in Greater Burlington, Vermont Area TownsDocument1 pagePopulation Growth in Greater Burlington, Vermont Area TownsCloverWhithamNo ratings yet

- Vermont Population From 2000 To 2017Document1 pageVermont Population From 2000 To 2017CloverWhithamNo ratings yet

- Income and Poverty in Vermont CountiesDocument1 pageIncome and Poverty in Vermont CountiesCloverWhithamNo ratings yet

- Turkey Labor Price GraphDocument1 pageTurkey Labor Price GraphCloverWhithamNo ratings yet

- Giving Season CouponDocument1 pageGiving Season CouponEmilie StiglianiNo ratings yet

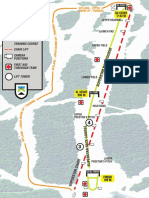

- Course Map For World Cup 2017 at Killington, VermontDocument1 pageCourse Map For World Cup 2017 at Killington, VermontCloverWhithamNo ratings yet

- No. Tipe Akun Kode Perkiraan NamaDocument6 pagesNo. Tipe Akun Kode Perkiraan Namapkm.sdjNo ratings yet

- Review of Related LiteratureDocument3 pagesReview of Related LiteratureEaster Joy PatuladaNo ratings yet

- Questionnaire On Influence of Role of Packaging On ConsumerDocument5 pagesQuestionnaire On Influence of Role of Packaging On ConsumerMicheal Jones85% (13)

- Second Statement: For The Purpose of Donor's Tax, A Stranger Is A Person Who Is Not ADocument2 pagesSecond Statement: For The Purpose of Donor's Tax, A Stranger Is A Person Who Is Not AAllen KateNo ratings yet

- Forbes - Tony ElumeluDocument8 pagesForbes - Tony ElumeluFanele Chester50% (2)

- S 5 Bba (HRM)Document2 pagesS 5 Bba (HRM)Anjali GopinathNo ratings yet

- Movies DatabaseDocument40 pagesMovies DatabasevatsonwizzluvNo ratings yet

- PM RN A4.Throughput CostingDocument5 pagesPM RN A4.Throughput Costinghow cleverNo ratings yet

- SAMPLEX A - Obligations and Contracts - Atty. Sta. Maria - Finals 2014Document2 pagesSAMPLEX A - Obligations and Contracts - Atty. Sta. Maria - Finals 2014Don Dela ChicaNo ratings yet

- Introduction to India's Oil and Gas IndustryDocument15 pagesIntroduction to India's Oil and Gas IndustryMeena HarryNo ratings yet

- Industrial Finance Corporation of India (Ifci)Document2 pagesIndustrial Finance Corporation of India (Ifci)sumit athwaniNo ratings yet

- CostSheetDocument6 pagesCostSheetsudhansu prasadNo ratings yet

- Bank LoansDocument54 pagesBank LoansMark Alvin LandichoNo ratings yet

- New-Doing: How Strategic Use of Design Connects Business With PeopleDocument53 pagesNew-Doing: How Strategic Use of Design Connects Business With PeopleHernán Moya ArayaNo ratings yet

- MCQs Financial AccountingDocument12 pagesMCQs Financial AccountingPervaiz ShahidNo ratings yet

- Indian Securities Market ReviewDocument221 pagesIndian Securities Market ReviewSunil Suppannavar100% (1)

- Agribusiness Development Program Starts HereDocument6 pagesAgribusiness Development Program Starts Herepriya singhNo ratings yet

- Portfoli o Management: A Project OnDocument48 pagesPortfoli o Management: A Project OnChinmoy DasNo ratings yet

- Enter Pen Eur ShipDocument7 pagesEnter Pen Eur ShipMuskan Rathi 5100No ratings yet

- NABARD financing pattern analysisDocument9 pagesNABARD financing pattern analysisFizan NaikNo ratings yet

- Bài Tập Và Đáp Án Chương 1Document9 pagesBài Tập Và Đáp Án Chương 1nguyenductaiNo ratings yet

- CPED Policy Brief Series 2021 No.2Document7 pagesCPED Policy Brief Series 2021 No.2Job EronmhonseleNo ratings yet

- Process Analysis: SL No Process Proces S Owner Input Output Methods Interfaces With Measure of Performance (MOP)Document12 pagesProcess Analysis: SL No Process Proces S Owner Input Output Methods Interfaces With Measure of Performance (MOP)DhinakaranNo ratings yet

- Industries: Growth and Problems of Major Industries 1. Iron & Steel 2. Cotton Textiles 3. Cement 4. Sugar 5. PetroleumDocument10 pagesIndustries: Growth and Problems of Major Industries 1. Iron & Steel 2. Cotton Textiles 3. Cement 4. Sugar 5. PetroleumvidhipoojaNo ratings yet

- Profits and Gains of Business or ProfessionDocument13 pagesProfits and Gains of Business or Professionajaykumar0011100% (2)

- The Economic ProblemDocument22 pagesThe Economic ProblemPeterNo ratings yet

- MITS5001 Project Management Case StudyDocument6 pagesMITS5001 Project Management Case Studymadan GaireNo ratings yet

- Customer Journey MappingDocument10 pagesCustomer Journey MappingpradieptaNo ratings yet

- SBR Open TuitionDocument162 pagesSBR Open TuitionpatrikosNo ratings yet

- American Rescue Plan - Ulster County Survey ResultsDocument2 pagesAmerican Rescue Plan - Ulster County Survey ResultsDaily FreemanNo ratings yet