You might also like

- Charitable TrustDocument2 pagesCharitable TrustvipingplNo ratings yet

- Massachussetts Business Trust - Law ReviewDocument36 pagesMassachussetts Business Trust - Law ReviewJulio Cesar NavasNo ratings yet

- Negotiable Instruments Case DigestDocument5 pagesNegotiable Instruments Case DigestCazzandhra BullecerNo ratings yet

- Non-Charitable Trusts NotesDocument6 pagesNon-Charitable Trusts NotesAgitha GunasagranNo ratings yet

- Affidavit For ArrestDocument2 pagesAffidavit For ArrestJefferson TanNo ratings yet

- Post-Petition Financing ProtectionsDocument9 pagesPost-Petition Financing ProtectionsSachin BhandawatNo ratings yet

- LeverageDocument38 pagesLeverageAnant MauryaNo ratings yet

- How California Trust Companies Function by L.H. RoseberryDocument7 pagesHow California Trust Companies Function by L.H. Roseberryreal-estate-historyNo ratings yet

- Replevin: (Sections 1-2, Rule 60, Rules of Court)Document10 pagesReplevin: (Sections 1-2, Rule 60, Rules of Court)Leo NekkoNo ratings yet

- Evolutionary Theory and The Origin of Property Rights PDFDocument22 pagesEvolutionary Theory and The Origin of Property Rights PDFKshitij PatilNo ratings yet

- Monthly Tax Return For Wagers: (Section 4401 of The Internal Revenue Code)Document4 pagesMonthly Tax Return For Wagers: (Section 4401 of The Internal Revenue Code)IRSNo ratings yet

- Indian Stamp Act Q&ADocument5 pagesIndian Stamp Act Q&ABrij NandanNo ratings yet

- Private School Affidavit Confirmation (CA Dept of EducationDocument5 pagesPrivate School Affidavit Confirmation (CA Dept of EducationDiaan100% (1)

- RelinquishDocument2 pagesRelinquishBilla NaganathNo ratings yet

- GiftDeedUnder40Document1 pageGiftDeedUnder40Rana Faisal Bashir PavarNo ratings yet

- G. M. Wagh - Property Law - Indian Trusts Act, 1882 (2021)Document54 pagesG. M. Wagh - Property Law - Indian Trusts Act, 1882 (2021)Akshata SawantNo ratings yet

- TRUSTEE - Docx Transfer Ing Property Trust To KevinDocument3 pagesTRUSTEE - Docx Transfer Ing Property Trust To KevinKevin Alspach100% (1)

- Crocker v. Malley, 249 U.S. 223 (1919)Document5 pagesCrocker v. Malley, 249 U.S. 223 (1919)Scribd Government DocsNo ratings yet

- United States Court of Appeals Ninth CircuitDocument7 pagesUnited States Court of Appeals Ninth CircuitScribd Government DocsNo ratings yet

- Registration Process of Public Charitable TrustDocument5 pagesRegistration Process of Public Charitable Trustpan RegisterNo ratings yet

- Registeringititling A Vehicle in New York StateDocument4 pagesRegisteringititling A Vehicle in New York StatehksdhfjkNo ratings yet

- Actual &V Constructive Legal NoticeDocument2 pagesActual &V Constructive Legal NoticeDarrell Wilson100% (2)

- F 8300Document5 pagesF 8300IRSNo ratings yet

- Understanding Taxation of Trust in IndiaDocument22 pagesUnderstanding Taxation of Trust in IndiaVipul DesaiNo ratings yet

- Steps For Issuing Dunning Letter To CustomerDocument4 pagesSteps For Issuing Dunning Letter To CustomerAnamika PandeyNo ratings yet

- Michigan Brewing Company Bankruptcy FilingDocument171 pagesMichigan Brewing Company Bankruptcy FilingLansingStateJournalNo ratings yet

- Choice Is YoursDocument23 pagesChoice Is Yoursffmaer100% (2)

- Request For Taxpayer Identification Number and CertificationDocument2 pagesRequest For Taxpayer Identification Number and Certificationdonald.price11306100% (1)

- I-864 Affidavit of Support PDFDocument12 pagesI-864 Affidavit of Support PDFO'sNachi De GeAntNo ratings yet

- Affidavit Mortgagee Bank PDFDocument1 pageAffidavit Mortgagee Bank PDFRanie DelaventeNo ratings yet

- Response To Resistance Collier County Sheriff's OfficeDocument4 pagesResponse To Resistance Collier County Sheriff's OfficeMichael BraunNo ratings yet

- A Trust Can Either Be A Private Trust or A Public Charitable TrustDocument2 pagesA Trust Can Either Be A Private Trust or A Public Charitable TrustShwetaHarlalkaNo ratings yet

- United States Court of Appeals, Eleventh CircuitDocument12 pagesUnited States Court of Appeals, Eleventh CircuitScribd Government DocsNo ratings yet

- Family Trust Q A For Download PDFDocument9 pagesFamily Trust Q A For Download PDFphil8984No ratings yet

- Non Disc Hold HarmDocument4 pagesNon Disc Hold HarmSylvester MooreNo ratings yet

- Corporation Law CasesDocument7 pagesCorporation Law CasesElerlenne LimNo ratings yet

- I-589 Anotaciones InglésDocument12 pagesI-589 Anotaciones InglésRod Peña Ray100% (1)

- Judicial Protection of Membership in Private AssociationsDocument16 pagesJudicial Protection of Membership in Private AssociationsBugout Zurvival100% (1)

- Bill of Lading Template PDFDocument1 pageBill of Lading Template PDFSakthivel PNo ratings yet

- Contract To SellDocument3 pagesContract To SellIan GermanNo ratings yet

- Contract of Adhesion - FinalDocument15 pagesContract of Adhesion - FinalDebashish DashNo ratings yet

- The Declaration of Independence: A Play for Many ReadersFrom EverandThe Declaration of Independence: A Play for Many ReadersNo ratings yet

- NEGOTIABLE INSTRUMENTS GUIDEDocument7 pagesNEGOTIABLE INSTRUMENTS GUIDEjustine cabanaNo ratings yet

- Trust Account Disbursement RequestDocument2 pagesTrust Account Disbursement Requestchristian09x100% (1)

- Trust ActDocument21 pagesTrust Actks136No ratings yet

- US Internal Revenue Service: f1041t - 1998Document2 pagesUS Internal Revenue Service: f1041t - 1998IRSNo ratings yet

- Tax Free Wealth 2019 Companion FileDocument27 pagesTax Free Wealth 2019 Companion FiledrodduqueNo ratings yet

- Trust and Estate OutlineDocument64 pagesTrust and Estate Outlineonly1mNo ratings yet

- PARTIES AND HOLDERS OF NEGOTIABLE INSTRUMENTSDocument2 pagesPARTIES AND HOLDERS OF NEGOTIABLE INSTRUMENTSRAJ BHAGATNo ratings yet

- Investment Income and Expenses: (Including Capital Gains and Losses)Document76 pagesInvestment Income and Expenses: (Including Capital Gains and Losses)Kenny Svatek100% (1)

- Constitution For An Unincorporated Non-Profit AssociationDocument4 pagesConstitution For An Unincorporated Non-Profit AssociationLegal Forms86% (7)

- Defamation PDFDocument3 pagesDefamation PDFRanjan BaradurNo ratings yet

- Preview 2780 2Document2 pagesPreview 2780 2Sylvester MooreNo ratings yet

- General BankingDocument167 pagesGeneral BankingSuvasish DasguptaNo ratings yet

- Last Will and Testament - Single Adult With Adult ChildrenDocument5 pagesLast Will and Testament - Single Adult With Adult Childrenaryabhave100% (1)

- Accies Trust Board Meeting Minutes - October 2009Document3 pagesAccies Trust Board Meeting Minutes - October 2009Accies TrustNo ratings yet

- Upload Bangladesh Affidavit of Identity FormDocument1 pageUpload Bangladesh Affidavit of Identity Formblack spicyNo ratings yet

- Charles Hewitt V Derrick Thompson LawsuitDocument11 pagesCharles Hewitt V Derrick Thompson LawsuitJames JusticeNo ratings yet

- Conveyance Deed: Stamps Issued To Challan No. - For Rs. - /-DatedDocument22 pagesConveyance Deed: Stamps Issued To Challan No. - For Rs. - /-Dateddecent4uNo ratings yet

- Audit Commands For FinacleDocument3 pagesAudit Commands For FinacleDavinder Kaur Oberoi100% (1)

- Tauras Mutual FundDocument13 pagesTauras Mutual Fundsandeep62No ratings yet

- Rokankaroni Pathshala (Investors SchoolDocument14 pagesRokankaroni Pathshala (Investors Schoolsandeep62No ratings yet

- Form Private Limited CompanyDocument2 pagesForm Private Limited Companysandeep62No ratings yet

- Parichay Pustika Mutual Fund PDFDocument37 pagesParichay Pustika Mutual Fund PDFVivek PatelNo ratings yet

- 37 Years Return Silver SensexDocument2 pages37 Years Return Silver Sensexsandeep62No ratings yet

- 37 Years Return FD SensexDocument2 pages37 Years Return FD Sensexsandeep62No ratings yet

- Finacle CBS FAQ GuideDocument38 pagesFinacle CBS FAQ Guidesandeep62No ratings yet

- Cash FlowDocument4 pagesCash Flowsandeep62No ratings yet

- 37 Years Return Gold SensexDocument2 pages37 Years Return Gold Sensexsandeep62No ratings yet

- Build Wealth With ConfidenceDocument16 pagesBuild Wealth With Confidencesandeep62No ratings yet

- LIC Is India's Most Attractive BFSI BrandDocument1 pageLIC Is India's Most Attractive BFSI Brandsandeep62No ratings yet

- Tot CotDocument6 pagesTot Cotsandeep62No ratings yet

- Draft Circular On Refunds in Service TaxDocument12 pagesDraft Circular On Refunds in Service Taxsandeep62No ratings yet

- CompanyListA FDocument291 pagesCompanyListA Fsandeep620% (1)

- Toibg 2012 2 2 2Document1 pageToibg 2012 2 2 2sandeep62No ratings yet

- Hosur-Phase-I Industrial Complex CompaniesDocument24 pagesHosur-Phase-I Industrial Complex Companiessridharcvlr67% (6)

- Unplanned RetirementDocument2 pagesUnplanned Retirementsandeep62No ratings yet

- Pharma Bulk1Document43 pagesPharma Bulk1sandeep620% (1)

- Payment of Gratuity The Payment of GratuityDocument4 pagesPayment of Gratuity The Payment of Gratuitysubhasishmajumdar100% (1)

- Archidply 2010Document44 pagesArchidply 2010Puneet367No ratings yet

- Price ListDocument2 pagesPrice Listsandeep62No ratings yet

- Revenue Memorandum Circular No. 35-06: June 21, 2006Document18 pagesRevenue Memorandum Circular No. 35-06: June 21, 2006dom0202No ratings yet

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument1 pageBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total Amountnupur.gaba97No ratings yet

- Progressive Proportional Tax ExplainedDocument28 pagesProgressive Proportional Tax ExplainedZARANo ratings yet

- Transfer TaxesDocument6 pagesTransfer TaxesRona Mae Ocampo Resare100% (2)

- Income Tax Trust EstatesDocument65 pagesIncome Tax Trust EstatesWeiwen Wang100% (1)

- Residential Status & Scope of Total IncomeDocument23 pagesResidential Status & Scope of Total IncomeKartikNo ratings yet

- Arn Receipt GST Rfd-01a 10ctupk3011q1zh ExbclDocument1 pageArn Receipt GST Rfd-01a 10ctupk3011q1zh ExbclRAHUL AGGARWALNo ratings yet

- A Synopsis ON "Study On Tax Planning of 10 Assesses"Document6 pagesA Synopsis ON "Study On Tax Planning of 10 Assesses"hemant100% (1)

- Appointment of Custom OfficerDocument3 pagesAppointment of Custom OfficerFatima TurkNo ratings yet

- 2010 ADSO As DGPA Tax ReturnDocument17 pages2010 ADSO As DGPA Tax ReturnDentist The MenaceNo ratings yet

- Payment Voucher (: Non-Instructional Staff)Document5 pagesPayment Voucher (: Non-Instructional Staff)Principal HanguNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon City Second DivisionDocument38 pagesRepublic of The Philippines Court of Tax Appeals Quezon City Second DivisionMaricon Bangalan-CanarejoNo ratings yet

- Onex I 230956Document2 pagesOnex I 230956chunduharikrishnaNo ratings yet

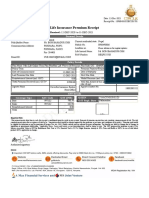

- Life Insurance Premium Receipt: Personal DetailsDocument1 pageLife Insurance Premium Receipt: Personal Detailschanam bedantaNo ratings yet

- Government AccountingDocument2 pagesGovernment AccountingLloyd SonicaNo ratings yet

- Capital Budgeting Seatwork 2 MWFDocument1 pageCapital Budgeting Seatwork 2 MWFnelle de leonNo ratings yet

- HDFC Life YoungStar Udaan IllustrationDocument2 pagesHDFC Life YoungStar Udaan IllustrationSuraj RajbharNo ratings yet

- Final Withholding Taxes Fringe Benefit TaxDocument27 pagesFinal Withholding Taxes Fringe Benefit Taxairwaller rNo ratings yet

- SEO-Optimized Title for Retail InvoiceDocument2 pagesSEO-Optimized Title for Retail InvoiceManish LahotiNo ratings yet

- 14 Grace: Practice QuestionsDocument1 page14 Grace: Practice QuestionsIvy NjorogeNo ratings yet

- FATCA Presentation - KhaledDocument42 pagesFATCA Presentation - KhaledMd.Aminul Islam BhuiyanNo ratings yet

- Capital GainsDocument8 pagesCapital GainsSarfaraz Singh LegaNo ratings yet

- House Company borrows $3.75M under financing agreementDocument4 pagesHouse Company borrows $3.75M under financing agreementCarlo ParasNo ratings yet

- Betwinner IO CPA 2Document2 pagesBetwinner IO CPA 2Arun KarthikNo ratings yet

- RI22507945 - Dec 28 2022 - 183245Document2 pagesRI22507945 - Dec 28 2022 - 183245vijayNo ratings yet

- VAT Guide: Rates, Returns, Filing ProceduresDocument33 pagesVAT Guide: Rates, Returns, Filing ProceduresvicsNo ratings yet

- 1617 1stS FX CLim 1 1Document10 pages1617 1stS FX CLim 1 1ShitzeoNo ratings yet

- CIR V BurmeisterDocument3 pagesCIR V BurmeisterGenevieve Kristine ManalacNo ratings yet

- Income Tax CalcDocument7 pagesIncome Tax Calckarthik.ragu9101No ratings yet

- Taxa7319 MoDocument50 pagesTaxa7319 MoarronyeagarNo ratings yet