You might also like

- Business Development Strategy for the Upstream Oil and Gas IndustryFrom EverandBusiness Development Strategy for the Upstream Oil and Gas IndustryRating: 5 out of 5 stars5/5 (1)

- Strategy, Value and Risk: A Guide to Advanced Financial ManagementFrom EverandStrategy, Value and Risk: A Guide to Advanced Financial ManagementNo ratings yet

- Home Mail News Finance Sports Entertainment Life Yahoo Plus MORE... Yahoo FinanceDocument49 pagesHome Mail News Finance Sports Entertainment Life Yahoo Plus MORE... Yahoo FinanceCasual ThingNo ratings yet

- Sector 2: Oil & Gas Company 1: BPCL General OverviewDocument5 pagesSector 2: Oil & Gas Company 1: BPCL General Overviewxilox67632No ratings yet

- Key Ratios For Analyzing Oil and Gas Stocks: Measuring Performance - InvestopediaDocument3 pagesKey Ratios For Analyzing Oil and Gas Stocks: Measuring Performance - Investopediapolobook3782No ratings yet

- Key Ratios For Analyzing Oil and Gas Stocks - Measuring PerformanceDocument3 pagesKey Ratios For Analyzing Oil and Gas Stocks - Measuring Performancek7hussainNo ratings yet

- M5.2 PepsiCo and Coca Cola PDFDocument4 pagesM5.2 PepsiCo and Coca Cola PDFKanika AhujaNo ratings yet

- Campbell's Soup ValuationDocument10 pagesCampbell's Soup ValuationsponerdbNo ratings yet

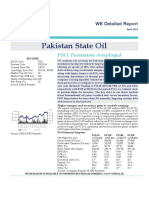

- PSO Detailed Report 2Document9 pagesPSO Detailed Report 2Javaid IqbalNo ratings yet

- In This StudyDocument3 pagesIn This StudyAhmad Al HajjarNo ratings yet

- ForbesDocument24 pagesForbesapi-330066158No ratings yet

- MiF - PE&VC - Group 1 - HertzDocument4 pagesMiF - PE&VC - Group 1 - HertzДмитрий КолесниковNo ratings yet

- DuPont PDFDocument5 pagesDuPont PDFMadhur100% (1)

- Chemical Industry AnalysisDocument4 pagesChemical Industry AnalysisArmyboy 1804No ratings yet

- Term ProjectDocument9 pagesTerm ProjectAhmad Al HajjarNo ratings yet

- Conocophillips (Cop) - 2007 Integrated Oil & Gas OutlookDocument4 pagesConocophillips (Cop) - 2007 Integrated Oil & Gas OutlookSaul StermanNo ratings yet

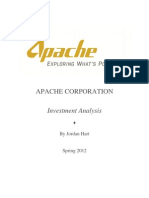

- Apache Corporation: Investment AnalysisDocument12 pagesApache Corporation: Investment AnalysisjordanchartNo ratings yet

- Letter To Gary Owen - BoD Geospace Technologies Corporation (NASDAQ: GEOS)Document6 pagesLetter To Gary Owen - BoD Geospace Technologies Corporation (NASDAQ: GEOS)amvonaNo ratings yet

- Pinnacle - Economics of Reliability - Global Refining 2022Document26 pagesPinnacle - Economics of Reliability - Global Refining 2022Bruno ZindyNo ratings yet

- BBBY Case ExerciseDocument7 pagesBBBY Case ExerciseSue McGinnisNo ratings yet

- BP Strategic and Financial AnalysisDocument25 pagesBP Strategic and Financial AnalysisBatu Cem EkizNo ratings yet

- Royal Dutch Shell and BG Group Case StudyDocument7 pagesRoyal Dutch Shell and BG Group Case StudyFattyschippy1No ratings yet

- Exxon and Mobil Fueling The World Safely and Responsibly: Nirmith Ps 21SJCCC467 3 Bcom EDocument29 pagesExxon and Mobil Fueling The World Safely and Responsibly: Nirmith Ps 21SJCCC467 3 Bcom ENIRMITH PSNo ratings yet

- Annual ReportDocument192 pagesAnnual ReporttsanshineNo ratings yet

- Oil Investing in An AntiDocument8 pagesOil Investing in An AntiAce NooneNo ratings yet

- British PetroleumDocument10 pagesBritish PetroleumVPrasarnth RaajNo ratings yet

- Rosete, Gherlen Clare A. Manacct Prof. Lopez Comparative AnalysisDocument8 pagesRosete, Gherlen Clare A. Manacct Prof. Lopez Comparative AnalysisGlare RoseteNo ratings yet

- Peters On Part 3Document18 pagesPeters On Part 3Michelle PetersonNo ratings yet

- Ejemplo Caso Financiera InglesDocument20 pagesEjemplo Caso Financiera Ingleselena wuNo ratings yet

- Final Valuation Report GSDocument8 pagesFinal Valuation Report GSGennadiy SverzhinskiyNo ratings yet

- Executive Summary: Getting Tired of Never-Ending Assignments?Document15 pagesExecutive Summary: Getting Tired of Never-Ending Assignments?Nam Nguyễn AnhNo ratings yet

- Cjenergy ValuationDocument11 pagesCjenergy Valuationapi-239586293No ratings yet

- Stocks To Buy: NewslettersDocument17 pagesStocks To Buy: Newslettersfrank valenzuelaNo ratings yet

- Sino Clean Energy - Investor Presentation - April 2011Document29 pagesSino Clean Energy - Investor Presentation - April 2011Sai RavishankarNo ratings yet

- Balance Sheet AnalysisDocument4 pagesBalance Sheet AnalysisArchit GuptaNo ratings yet

- RIL Macquarie 10 July 06Document50 pagesRIL Macquarie 10 July 06alokkuma05No ratings yet

- TermDocument4 pagesTermAhmad Al HajjarNo ratings yet

- Nova Chemical CorporationDocument28 pagesNova Chemical Corporationrzannat94100% (2)

- Barclays Back To School Consumer ConferenceDocument37 pagesBarclays Back To School Consumer ConferenceBrian FanneyNo ratings yet

- Company AnalysisDocument20 pagesCompany AnalysisRamazan BarbariNo ratings yet

- Capm AnalysisDocument18 pagesCapm Analysisnadun sanjeewaNo ratings yet

- BP FinalDocument20 pagesBP FinalPratik BhagatNo ratings yet

- Example MidlandDocument5 pagesExample Midlandtdavis1234No ratings yet

- Analiza Premierfoods - Dec11Document3 pagesAnaliza Premierfoods - Dec11Tudor OprisorNo ratings yet

- DuPont Corporation - Sale of Performance CoatingsDocument8 pagesDuPont Corporation - Sale of Performance CoatingsPeterNo ratings yet

- Shell Case StudyDocument3 pagesShell Case StudyJhon RamosNo ratings yet

- BP S: C F M: Aftermath OF OIL Pill Orporate Inancial AnagementDocument12 pagesBP S: C F M: Aftermath OF OIL Pill Orporate Inancial AnagementprofessionalwritersNo ratings yet

- PolarSports Solution PDFDocument8 pagesPolarSports Solution PDFaotorres99No ratings yet

- Group Project - Sensitivity AnalysisDocument8 pagesGroup Project - Sensitivity AnalysisSalomon Cure CorreaNo ratings yet

- Outlook - Energy-Cross-Region - 26apr21 MoodysDocument10 pagesOutlook - Energy-Cross-Region - 26apr21 MoodysPedro MentadoNo ratings yet

- Loblaws Writting SampleDocument5 pagesLoblaws Writting SamplePrakshay Puri100% (1)

- Running Head: Environmental Scan and Financial Analysis 1Document7 pagesRunning Head: Environmental Scan and Financial Analysis 1brunoNo ratings yet

- Looking To The Future PDFDocument8 pagesLooking To The Future PDFHadiBiesNo ratings yet

- Kitchen Ware SolutionDocument6 pagesKitchen Ware SolutionIrfan ShaikhNo ratings yet

- ExxonMobil Analysis ReportDocument18 pagesExxonMobil Analysis Reportaaldrak100% (2)

- FMA Assignment 1Document11 pagesFMA Assignment 1naconrad1888No ratings yet

- "Financial Analysis of Kilburn Chemicals": Case Study OnDocument20 pages"Financial Analysis of Kilburn Chemicals": Case Study Onshraddha mehtaNo ratings yet

- Royalty Review 0815 BMO (00000002)Document25 pagesRoyalty Review 0815 BMO (00000002)TeamWildroseNo ratings yet

- BP Strong BuyDocument3 pagesBP Strong BuysinnlosNo ratings yet

- Corporate Finance Coca ColaDocument13 pagesCorporate Finance Coca ColaSchwalbe TRNo ratings yet

- Vanguard Industrials EtfDocument2 pagesVanguard Industrials Etfapi-269271900No ratings yet

- Joel Prather Letter of Reference CPDDocument1 pageJoel Prather Letter of Reference CPDapi-269271900No ratings yet

- To Whom It May ConcernDocument1 pageTo Whom It May Concernapi-269271900No ratings yet

- Recommendation Joel PratherDocument1 pageRecommendation Joel Pratherapi-269271900No ratings yet

- Values QuestionnaireDocument1 pageValues Questionnaireapi-269271900No ratings yet

- My RésuméDocument1 pageMy RésuméjcpratherNo ratings yet

- Unit 6 Selected and Short AnswersDocument19 pagesUnit 6 Selected and Short Answersbebepic355No ratings yet

- Application List: Required Items: A: Cpu-95 Ignition ModuleDocument12 pagesApplication List: Required Items: A: Cpu-95 Ignition ModuleShubra DebNo ratings yet

- Irjet V3i7146 PDFDocument6 pagesIrjet V3i7146 PDFatulnarkhede2002No ratings yet

- Symantec Endpoint Protection 14.3 RU3 Release NotesDocument28 pagesSymantec Endpoint Protection 14.3 RU3 Release NotesMilind KuleNo ratings yet

- Samsung LN55C610N1FXZA Fast Track Guide (SM)Document4 pagesSamsung LN55C610N1FXZA Fast Track Guide (SM)Carlos OdilonNo ratings yet

- What Is E-CollaborationDocument7 pagesWhat Is E-CollaborationToumba LimbreNo ratings yet

- D904 - D906 - D914 - D916 - D924 - D926 - 8718458 - 04092008 - v02 - enDocument218 pagesD904 - D906 - D914 - D916 - D924 - D926 - 8718458 - 04092008 - v02 - enАлексей89% (18)

- Structure of An Atom Revision PaperDocument5 pagesStructure of An Atom Revision PaperZoe Kim ChinguwaNo ratings yet

- CH 3 TestDocument50 pagesCH 3 TestVK ACCANo ratings yet

- FYP List 2020 21RDocument3 pagesFYP List 2020 21RSaif UllahNo ratings yet

- Former Rajya Sabha MP Ajay Sancheti Appeals Finance Minister To Create New Laws To Regulate Cryptocurrency MarketDocument3 pagesFormer Rajya Sabha MP Ajay Sancheti Appeals Finance Minister To Create New Laws To Regulate Cryptocurrency MarketNation NextNo ratings yet

- Tele-Medicine: Presented by Shyam.s.s I Year M.SC NursingDocument12 pagesTele-Medicine: Presented by Shyam.s.s I Year M.SC NursingShyamNo ratings yet

- Marketing Research Completed RevisedDocument70 pagesMarketing Research Completed RevisedJodel DagoroNo ratings yet

- Nur Syamimi - Noor Nasruddin - Presentation - 1002 - 1010 - 1024Document14 pagesNur Syamimi - Noor Nasruddin - Presentation - 1002 - 1010 - 1024abdulhasnalNo ratings yet

- Culture NegotiationsDocument17 pagesCulture NegotiationsShikha SharmaNo ratings yet

- Nail Malformation Grade 8Document30 pagesNail Malformation Grade 8marbong coytopNo ratings yet

- Bashar CitateDocument7 pagesBashar CitateCristiana ProtopopescuNo ratings yet

- Optimizing Patient Flow: Innovation Series 2003Document16 pagesOptimizing Patient Flow: Innovation Series 2003Jeff SavageNo ratings yet

- Term Paper Gender RolesDocument5 pagesTerm Paper Gender Rolesea8d1b6n100% (1)

- CNL DivisionDocument38 pagesCNL DivisionaniketnareNo ratings yet

- State Partnership Program 101 Brief (Jan 2022)Document7 pagesState Partnership Program 101 Brief (Jan 2022)Paulo FranciscoNo ratings yet

- University of Dar Es Salaam: Faculty of Commerce and ManagementDocument37 pagesUniversity of Dar Es Salaam: Faculty of Commerce and ManagementEric MitegoNo ratings yet

- THE FIELD SURVEY PARTY ReportDocument3 pagesTHE FIELD SURVEY PARTY ReportMacario estarjerasNo ratings yet

- Facility Layout Case StudyDocument8 pagesFacility Layout Case StudyHitesh SinglaNo ratings yet

- Jahnteller Effect Unit 3 2017Document15 pagesJahnteller Effect Unit 3 2017Jaleel BrownNo ratings yet

- Hal Foster Vision and Visuality Discussions in Contemporary Culture PDFDocument75 pagesHal Foster Vision and Visuality Discussions in Contemporary Culture PDFEd GomesNo ratings yet

- Competency #14 Ay 2022-2023 Social StudiesDocument22 pagesCompetency #14 Ay 2022-2023 Social StudiesCharis RebanalNo ratings yet

- Research PaperDocument14 pagesResearch PaperNeil Jhon HubillaNo ratings yet

- IGCSE Religious Studies (Edexcel - 2009 - Be Careful Not To Choose The New' IGCSE)Document8 pagesIGCSE Religious Studies (Edexcel - 2009 - Be Careful Not To Choose The New' IGCSE)Robbie TurnerNo ratings yet

- New Life in Christ - Vol05 - Engl - Teacher GuideDocument29 pagesNew Life in Christ - Vol05 - Engl - Teacher GuideOliver Angus100% (1)