You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Extras de Cont / Account: 2. Valuta / Currency 3. Data Extras / Statement DateDocument2 pagesExtras de Cont / Account: 2. Valuta / Currency 3. Data Extras / Statement Dateesseesse76100% (3)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Internal Audit Checklist of Scrap MaterialDocument1 pageInternal Audit Checklist of Scrap MaterialVijay Kumar Varanasi0% (1)

- Un Gse Form 100 F 05 04 2014Document3 pagesUn Gse Form 100 F 05 04 2014api-205109186No ratings yet

- Cvac OutlineDocument5 pagesCvac Outlineapi-205109186100% (2)

- Chemtrails Chemistry Manual Usaf Academy 1999Document202 pagesChemtrails Chemistry Manual Usaf Academy 1999api-205109186No ratings yet

- COC - SUbcontract FormDocument32 pagesCOC - SUbcontract Formsham2000No ratings yet

- Bank Statement EditedDocument4 pagesBank Statement EditedAllen MedinaNo ratings yet

- Protector Oath Bond 9-14-13Document2 pagesProtector Oath Bond 9-14-13api-205109186No ratings yet

- Public Servant Oath Bond 9-14-13Document2 pagesPublic Servant Oath Bond 9-14-13api-205109186No ratings yet

- 1998ndaa National Do Not Spray Me or Weather Modify Me List v1 DraftDocument17 pages1998ndaa National Do Not Spray Me or Weather Modify Me List v1 Draftapi-205109186100% (1)

- Data Sheet tg33k213t 3 12 13Document2 pagesData Sheet tg33k213t 3 12 13api-205109186No ratings yet

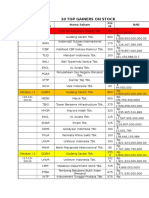

- 10 Top Gainers On Stock: Bulan/Min Ggu Kode Saham Nama Saham Poi NT NABDocument6 pages10 Top Gainers On Stock: Bulan/Min Ggu Kode Saham Nama Saham Poi NT NABFajRin WiCaksonoNo ratings yet

- Mercantile Law Past Papers PDFDocument60 pagesMercantile Law Past Papers PDFMuhammad YahyaNo ratings yet

- Acct Statement - XX4811 - 11032024Document21 pagesAcct Statement - XX4811 - 11032024amolgorkhe612No ratings yet

- PolicySoftCopy 102426488 PDFDocument3 pagesPolicySoftCopy 102426488 PDFAnbarasu sNo ratings yet

- United States Bankruptcy Court Southern District of New YorkDocument13 pagesUnited States Bankruptcy Court Southern District of New YorkChapter 11 DocketsNo ratings yet

- G Receipt VoucherDocument14 pagesG Receipt VoucherAqram Othman100% (1)

- Micro Finance KothariDocument21 pagesMicro Finance KothariKokila AmbigaeNo ratings yet

- CV Emmanuel ClaessensDocument1 pageCV Emmanuel ClaessensAnonymous 67Gz377rsANo ratings yet

- American Home VS TantucoDocument1 pageAmerican Home VS Tantucoiamnumber_fourNo ratings yet

- Ref - No. 4857458-15788895-3: Sharafat AliDocument4 pagesRef - No. 4857458-15788895-3: Sharafat AliYash RajpalNo ratings yet

- ALLSTATE The Darker Side 2010 CondensedDocument11 pagesALLSTATE The Darker Side 2010 CondensedSarah Watson100% (1)

- JuneDocument14 pagesJuneVikas K JainNo ratings yet

- Assertions in The Audit of Financial StatementsDocument3 pagesAssertions in The Audit of Financial StatementsBirei GonzalesNo ratings yet

- As 4910-2002 (Reference Use Only) General Conditions of Contract For The Supply of Equipment With InstallatioDocument7 pagesAs 4910-2002 (Reference Use Only) General Conditions of Contract For The Supply of Equipment With InstallatioSAI Global - APAC100% (1)

- Ar Questions in Negotiable InstrumentDocument9 pagesAr Questions in Negotiable InstrumentAtty AnnaNo ratings yet

- 01 - Model Curriculum - BCBF - 23122015Document8 pages01 - Model Curriculum - BCBF - 23122015Ashutosh Workaholic MishraNo ratings yet

- How To Apply For Puduvai Bharathiar Grama Bank Recruitment 2015-2016 For Clerk PostDocument2 pagesHow To Apply For Puduvai Bharathiar Grama Bank Recruitment 2015-2016 For Clerk PostprivatejobshubNo ratings yet

- Annual Report 2005 06Document70 pagesAnnual Report 2005 06mrkeralaNo ratings yet

- 5CD First Integrated Bonding Vs HernandoDocument1 page5CD First Integrated Bonding Vs HernandoMilcah MagpantayNo ratings yet

- Navig8 Almandine - Inv No 2019-002 - Santa Barbara Invoice + Voucher PDFDocument2 pagesNavig8 Almandine - Inv No 2019-002 - Santa Barbara Invoice + Voucher PDFAnonymous MoQ28DEBPNo ratings yet

- PRESENTATION On Merchant BankingDocument12 pagesPRESENTATION On Merchant Bankingsarthak1826No ratings yet

- Chief Executive Officer President in Minneapolis ST Paul MN Resume Gregory GottsackerDocument3 pagesChief Executive Officer President in Minneapolis ST Paul MN Resume Gregory GottsackerGregoryGottsacker100% (1)

- Choa Tiek Seng Vs CADocument1 pageChoa Tiek Seng Vs CAEarl LarroderNo ratings yet

- Revealed: Federal Reserve Asking CIT Group About Inner City Press FOIA Request: Now Goldman Sachs?Document40 pagesRevealed: Federal Reserve Asking CIT Group About Inner City Press FOIA Request: Now Goldman Sachs?Matthew Russell LeeNo ratings yet

- Inventories: Assertions Audit Objectives Audit Procedures I. Existence/ OccurrenceDocument4 pagesInventories: Assertions Audit Objectives Audit Procedures I. Existence/ OccurrencekrizzmaaaayNo ratings yet

- Iht205 2006 2Document4 pagesIht205 2006 2pacecurranbtinternetNo ratings yet